Trading in Spot, Forward, Futures, and Options Markets

In commodity trading, understanding the theoretical mechanisms of different markets is essential, but seeing these concepts applied in real-world scenarios is what truly brings them to life. This chapter will explore practical examples of how businesses and traders use spot, forward, futures, and options markets to achieve their goals, manage risks, and capitalize on opportunities.

1. Trading in the Spot Market

Example: Coffee Buyer Securing Immediate Supply

A coffee roastery in London is known for its commitment to offering freshly roasted coffee sourced from Cuba. Due to a sudden surge in customer demand, the roastery needs to purchase additional coffee beans immediately. The owner turns to the spot market, where commodities are bought and sold for immediate delivery.

Application:

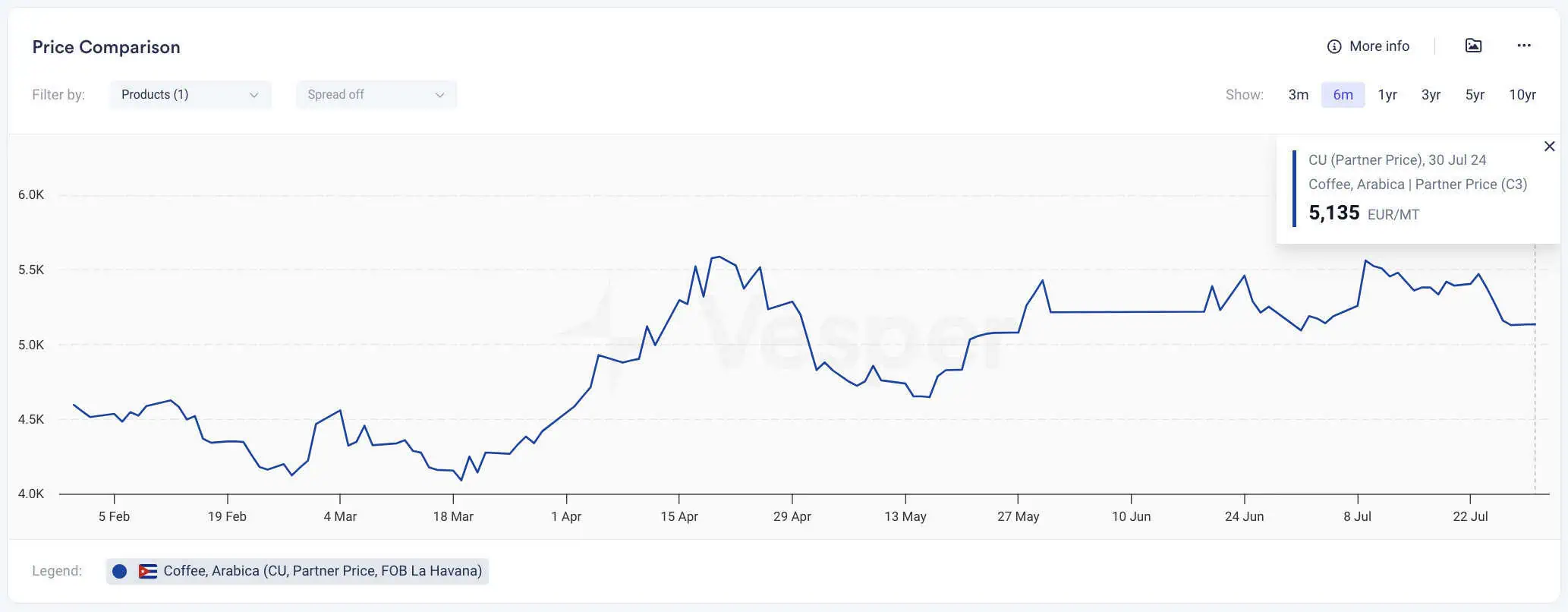

Before contacting the supplier in Cuba, the owner checks Vesper’s real-time price data for Arabica coffee. As shown in the price comparison graph below, Vesper provides up-to-date information on the partner price for Coffee Arabica (C3), which on 30 July 2024 was EUR 5,135 per metric tonne.

By leveraging Vesper’s data, the roastery owner gains a clear understanding of current price trends and fluctuations over the past six months. Observing that prices have stabilized after peaking in April, the owner feels confident in negotiating a price close to EUR 5,135 per metric tonne for the 10 metric tonnes of Arabica coffee beans. With this market intelligence, the owner contacts the Cuban supplier through an online spot market platform and successfully negotiates a competitive price based on the most recent data from Vesper.

Vesper’s data empowers the roastery owner to secure favourable pricing. The transaction is settled within days, ensuring that the coffee beans are delivered promptly, allowing the roastery to meet the increased demand. The spot market’s simplicity and speed are ideal in this situation, enabling the business to maintain its supply chain without any delays.

2. Trading in the Forward Market

Example 1: Wheat Buyer Securing Future Supply

A wheat buyer in France anticipates a need for a significant quantity of wheat in six months but is concerned about rising prices due to potential supply chain disruptions or geopolitical factors. To secure a stable price and protect against further increases, the buyer enters into a forward contract with a wheat producer.

Application:

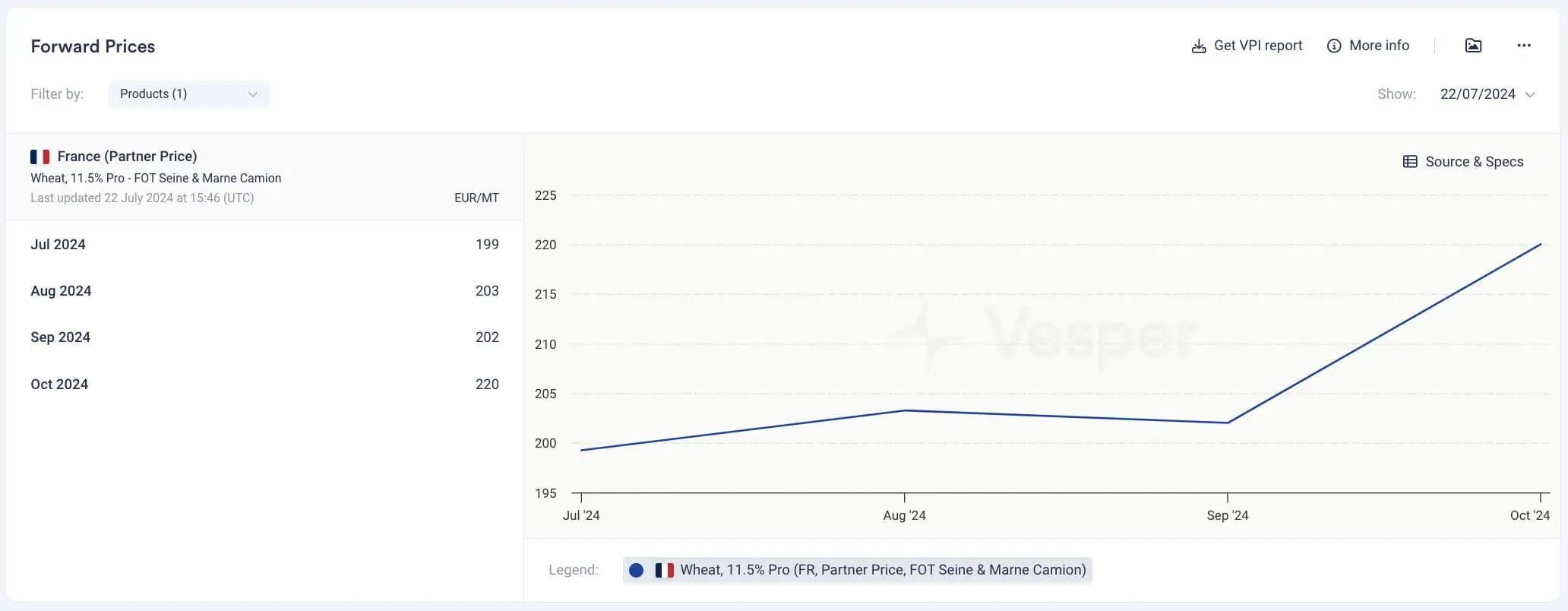

The buyer and the producer agree to a forward contract where the buyer will purchase 1,000 metric tonnes of wheat at a set price of EUR 203 per metric tonne in six months, as indicated by the forward price data from July 2024, see Figure below.

This forward contract is privately negotiated between the two parties and is customized to their specific needs, including the quantity, quality, and delivery date of the wheat. Unlike futures contracts, forward contracts are not traded on an exchange and are typically settled at maturity, meaning the actual delivery of the wheat and the payment occur at the end of the six-month period.

By locking in the price now, the buyer mitigates the risk of even higher prices in the future, ensuring a predictable cost for the wheat supply. This helps the buyer manage budgeting and pricing strategies more effectively. However, this arrangement also introduces counterparty risk, where either party could default on the agreement.

Example 2: Wheat Producer Locking in Future Prices

A US wheat producer anticipates a good harvest in six months but is concerned about potential price declines due to an expected bumper crop nationwide. To secure a favourable price, the producer enters into a forward contract with a local purchaser.

Application:

The producer and the purchaser agree to a forward contract where the producer will deliver 1,000 bushels of wheat at a set price of $5 per bushel in six months. This forward contract is privately negotiated between the two parties and is customised to their specific needs, including the quantity, quality, and delivery date of the wheat. Unlike futures contracts, forward contracts are not traded on an exchange and are typically settled at maturity, meaning the actual delivery of the wheat and the payment occur at the end of the six-month period.

This allows both parties to manage their risks and costs according to their specific requirements, but it also introduces counterparty risk, where either party could default on the agreement.

3. Trading in the Futures Market

Example: Airline Hedging Against Fuel Price Volatility

A major airline anticipates a rise in jet fuel prices due to geopolitical tensions in oil-producing regions. To protect against this risk, the airline’s risk manager decides to hedge by purchasing futures contracts for crude oil, which is the primary component of jet fuel.

Application:

The risk manager buys crude oil futures contracts for delivery in six months at 0.2590 USD/lb on the Intercontinental Exchange (ICE) EU. These futures contracts are standardised agreements that specify the quantity, quality, and delivery date of crude oil. Unlike forward contracts, futures are traded on an exchange and come with daily settlement of gains and losses, known as mark-to-market. This means that if the price of crude oil fluctuates, the value of the futures contract is adjusted daily, and the airline’s account is credited or debited accordingly. If oil prices rise to 0.2650 USD/lb as expected, see figure below, the airline benefits from the futures contract by paying the lower locked-in price of 0.2590 USD/lb, thereby reducing the impact of increased fuel costs on its operations. This use of futures contracts helps the airline manage its costs predictably, even in a volatile market.

4. Trading in the Options Market

Example: Corn Producer Speculating on Price Movements

A corn producer in Iowa is concerned about potential price declines but also wants to benefit from any upward price movements during the upcoming growing season. The producer opts for the flexibility of options as a speculative and protective strategy.

Application:

The producer purchases options on corn with a strike price of $4.00 per bushel, expiring in six months. The premium paid for this option is $0.20 per bushel. If corn prices fall to $3.50 per bushel before the expiration date, the producer can exercise the option, selling corn at the higher strike price of $4.00 per bushel, thereby offsetting the lower market prices. If the price rises above $4.00, the producer benefits from the higher market prices and simply lets the option expire, only losing the premium paid. This strategy allows the producer to hedge against potential losses while retaining the opportunity to benefit from favourable price increases.

Conclusion

Whether it’s a coffee roastery securing immediate supply, a producer locking in prices, an airline hedging against fuel costs, or a producer speculating on corn prices, the applications of these trading mechanisms are vast and varied. Understanding these applications not only deepens your knowledge of commodity markets but also equips you with practical insights for navigating these markets effectively.