The biggest change in US butter is easy to miss in the price. It shows up in the warehouse. The United States now exports more butter than it imports, a first, and its cold storage has run below year-ago levels every month of 2026. The country is making more butter than ever. It still cannot keep its own shelves as full as last year. The surplus is real. It is just leaving the country.

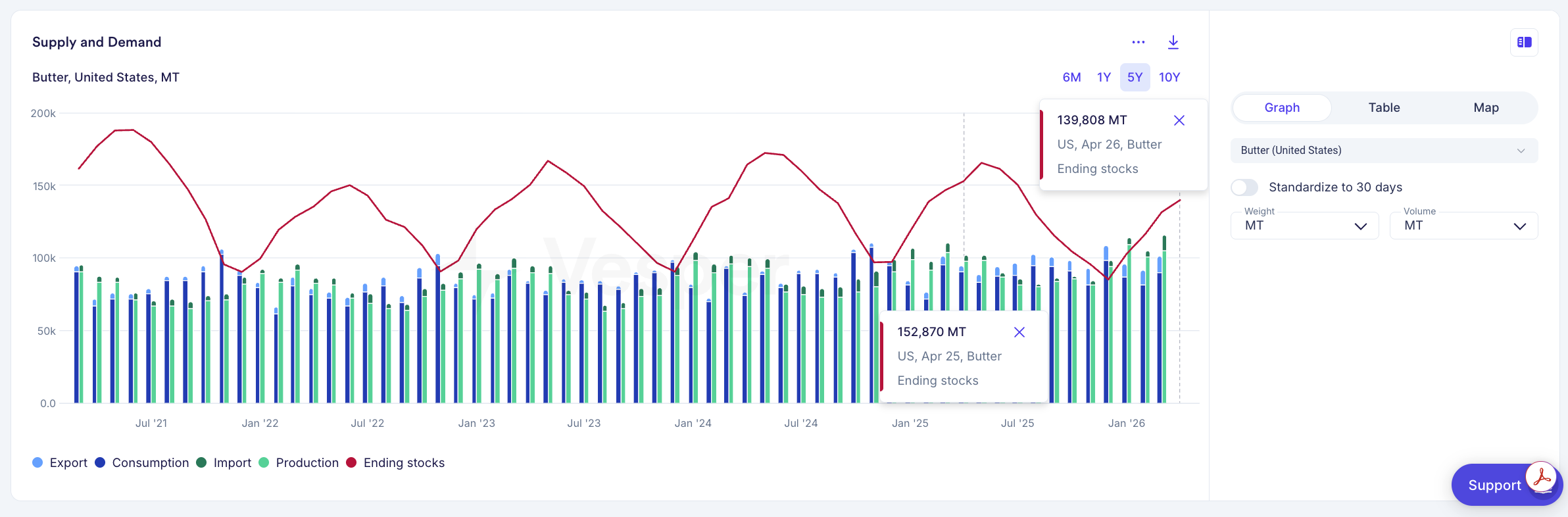

Start with the warehouse, because that is where the story is clearest. US butter ending stocks sat below the prior year in every month from December through April. December ran about 12% under, the gap widened to roughly 16% in February, then eased to about 8.5% by April. In plain numbers, April closed at 139,808 MT against 152,870 MT a year earlier. Butter stocks are seasonal, they build into summer and draw down over winter, so the comparison that matters is same month against same month. On that basis the 2026 line sits below 2025 the whole way around.

US butter ending stocks, MT. The 2026 line runs below 2025 at every month, 139,808 MT in April versus 152,870 MT a year earlier, an 8.5% deficit even as production hit records.

None of that came from weak production. Output rose 5.68% in 2025, an extra 27 million pounds, and first-quarter 2026 production was up 7.1% on the year. The churns have been busy. The milk has been there. The shortfall is on the demand side, and it comes from three directions at once.

Exports do most of the work, and they are the reason the US flipped. Butterfat exports more than doubled in 2025, up 166%, with November and December setting record months. Once US butter became the cheapest in the world, trade routes opened that the market had never used: Canada up 48% to $210 million, Saudi Arabia up more than fiftyfold in value, Bahrain up 1,788%, the Netherlands from near zero to a real number. A country that used to buy Irish butter is now shipping to the Gulf.

Domestic demand takes the rest.

The same low prices that opened the export lanes pulled buyers in at home. Butter has traded under $2/lb for most of the past year and slipped toward $1.50 by late May, after starting 2025 near $1.30/lb. Cheap butter is its own form of demand, and recipes that had moved to vegetable oils started moving back. Government buying adds a smaller, stubborn piece on top: USDA Section 32 purchases put about $75 million into butter in late February, demand that does not bend to price.

Put those together and the price stops being a reliable signal of supply. Butter at $1.50 looks like a glut. It is the reason the shelves stay tight. Cold storage is what is left after every buyer, foreign and domestic, has taken their share, and through the first half of 2026 they kept taking more than a record could cover.

The shift is structural now, not seasonal. First-quarter figures show production up 7.1%, consumption up 3.8%, and net exports clearly positive. Full-year data confirm the flip from net importer to net exporter. The first clean sign came back in January, when stocks first opened a double-digit gap to the year before and the open question was whether it would close. It did not. It narrowed, but it held, and the reason it held is the same reason it opened.

For a procurement team, that is the lesson worth keeping. Record production does not guarantee availability, and watching output without watching consumption and exports gives a false sense of comfort. When a country turns from net importer to cost-competitive exporter, the change lands hard on domestic buyers, because volume that used to stay home now leaves, and it does not go gradually. A 166% jump in exports is a step change, not a drift. And cheap does not mean loose. The cheapest butter in the world still needs a buyer, and when it finds enough of them, it stops being cheap.

The US butter market moves fast. Every week brings new cold storage data, production figures, export volumes, and cream pricing, and each one reshapes the picture.

Our US Weekly tracks all of it: butter, cheese, whey, NFDM, milk production, and the global forces pulling US dairy prices in every direction. Written by Vesper’s dairy team, in your inbox every Friday.