While every other US dairy commodity collapsed in 2025, whey proteins went the opposite direction. WPI broke $10/lb for the first time. WPC80 hit all-time highs. Chinese tariffs rerouted entire supply chains overnight. And demand just kept climbing.

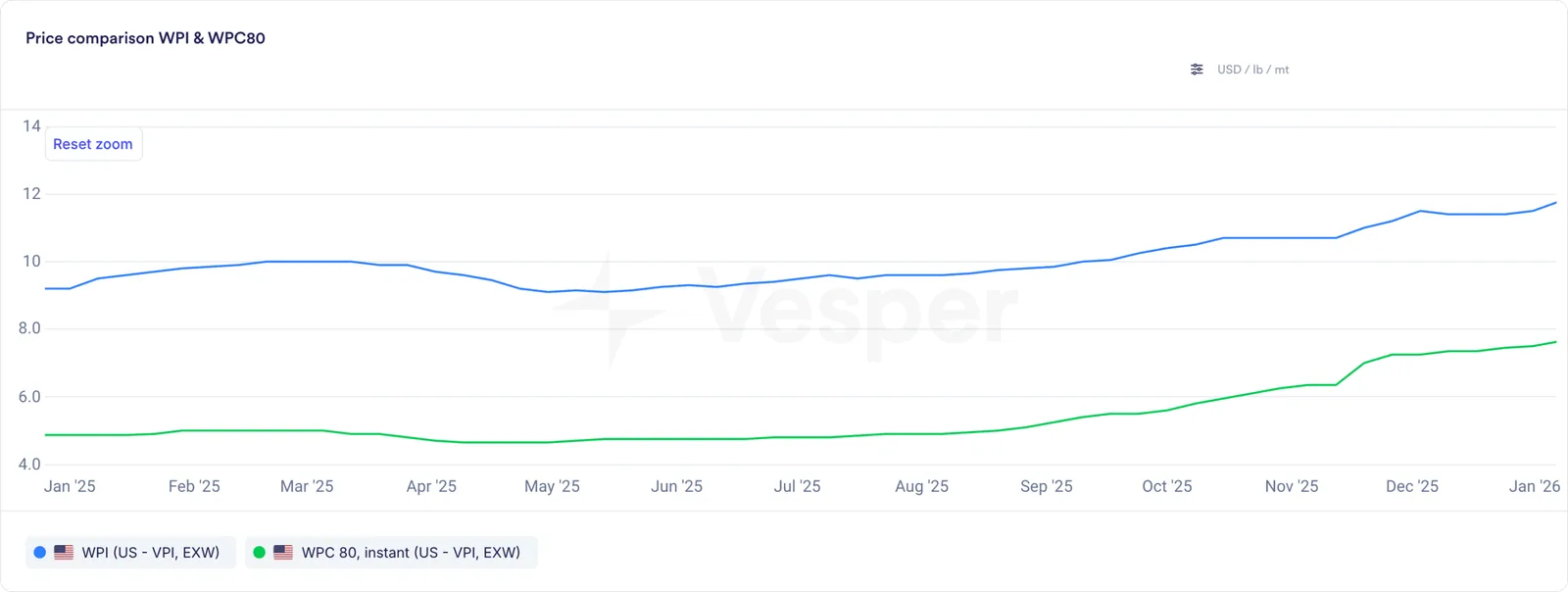

US WPI and WPC80 instant prices according to the Vesper Price Index in USD/lb (2025)

This is the story of the commodity that didn’t follow the script.

The setup: January 2025

WPI hit $9.5/lb in January and didn’t look back.

To put that in perspective: 3.5 lbs of butter cost the same as 1 lb of WPI. That’s a 179% price increase over 18 months.

Your first instinct: someone should be screaming. Customers should be walking away. Products should be getting discontinued.

That’s not what happened.

Sports nutrition brands absorbed the costs. They cut margins. They negotiated volume discounts. They stayed put. Whey was becoming non-negotiable.

Why? Because protein had become the default upgrade path for consumer packaged goods. Not the luxury add-on. The baseline.

WPI and WPC80 showed up everywhere in 2025: protein drinks, yogurts, puddings, shakes, meal replacements, bars, ice cream, lemonades, cookies, pancakes, infant formula, coffee. Every mainstream product got the protein treatment.

The numbers bore this out. Monthly whey protein consumption was now exceeding current stock levels. The market was tight. And traders kept saying the same thing: this tightness is here to stay.

February: Price discovery mode

WPI approached $10/lb by February. One trader’s quip summed up the mood: “Should be labeled as a precious metal.”

WPI wasn’t traded like a commodity anymore. It was in price discovery mode. Nobody quite knew the ceiling.

But here’s what matters for procurement teams: alternatives existed.

WPC80 was favorable. MPI85 was an option. MPI90 showed promise. All offered better value math.

The problem: consumers hadn’t switched. Brands had formulated products around WPI. Changing protein sources meant changing the product. That meant new testing, new approvals, new regulatory filings, new shelf documentation. The switching costs were real.

So brands stayed. And prices kept rising.

March: Tariffs enter the market

In March, China placed a 10% tariff on higher proteins.

This sounds small. It wasn’t.

Germany and the US are the dominant WPC80+ suppliers to China. EU WPI and WPC80 already showed small premiums over US proteins. But a 10% tariff on US shipments flipped the dynamics overnight.

US proteins became premium-priced in China. Chinese buyers faced a choice: pay more for US supply or shift to EU suppliers who were already price-competitive on the tariff-free side of the border.

The EU had tight protein supplies already. Now they faced additional demand pressure from China.

The arbitrage was about to break something.

April: Retaliation and production shifts

Tariff escalation continued. The US imposed approximately 145% tariffs on Chinese goods. China retaliated with 84% duties on US products.

China was taking 67 million pounds of higher proteins out of a 195 million pound US export base.

That’s the amount US producers counted on. Suddenly, it was gone.

US lost price competitiveness against European suppliers. And something unexpected happened on the production side.

WPI production jumped 19.91% year-over-year in February.

WPC80 production dropped 7.54%.

Producers were voting with their equipment. WPI hit higher prices. WPI got the investment. WPC80 got deprioritized.

May: Historic spreads

The EU-US protein spread blew out to levels nobody had seen before.

EU WPI showed a $1.83/lb premium over US supply in April. That’s 4x the 3-year historical average of $0.25/lb.

EU WPC80 hit a $1.58/lb premium. Again, 4x the historical average.

Chinese demand had pulled to Europe. But here’s where it got interesting: there was massive arbitrage sitting on the table.

US WPC80 was “landing” in Europe at EUR 11,000/mt. European domestic prices were EUR 12,000/mt. That’s a EUR 1,000/mt gap. Traders were eyeing it.

The spreads were historically wide. And they wouldn’t close quickly.

June: Partial correction, Persistent confusion

The EU-US WPI spread came down from $1.83/lb to $1.08/lb. Good news. But still 4x the 3-year average of $0.25/lb.

The WPC80 spread barely moved: $1.51/lb versus the 3-year average of $0.39/lb.

Three factors kept the spreads high.

First, the US still faced the 10% China tariff. That wasn’t going away.

Second, elevated prices create wider absolute spreads. When WPI is $10/lb instead of $6/lb, even a 10% variance is $1/lb instead of $0.60/lb.

Third, euro-dollar moves added 10%+ of their own volatility on top.

The spreads didn’t feel like arbitrage anymore. They felt structural.

July: The market splits in two

Observers started talking about the US whey market “splitting in two.”

High-protein products (WPC80, WPI) were trading at prices 3x historical lows on a 5-year chart. Which sounds like they crashed. They hadn’t. They were at all-time highs.

The confusion: “lows” versus “highs” depends on your baseline. Compared to their 2025 peaks, they were down. Compared to history, they were stratospheric.

Low-protein products (dry whey, lactose, permeate) were at rock bottom. Massive uncertainty. Nobody knew what happened to the 67 million pounds of US protein that China rejected.

Every price dip in high-proteins triggered immediate buying. GLP-1 diet trends were creating a new normal. Demand was inelastic.

Tariff uncertainty hung over most major US whey export destinations.

August: New Zealand gains, Germany dominates China

NZ WPC80+ exports to the US hit a record 2 million pounds in June. That’s double year-over-year.

In China, something more dramatic happened. Germany overtook the US as China’s top higher-protein supplier.

German WPC80+ imports to China were up 209% year-to-date. US exports to China were down 10.9% year-to-date.

But there was an offset: US domestic demand was strong. The lost China volume was getting absorbed by US manufacturers instead.

September: Parity, Then inversion

By September, WPC80 and WPI were keeping the entire whey spectrum supported.

Global buyers lined up for US WPC80 at discounts to Europe. US instant WPC80 traded at $5.80/lb. That was a record.

US WPI hit $10.50/lb. For the first time in the year, it traded above European prices at $10.33/lb.

The inversion mattered. It meant US supply was preferred again despite the tariff headwind.

But milk proteins weren’t benefiting equally. Milk protein concentrate and isolates were stuck while whey proteins soared.

The spread between milk and whey proteins hit all-time highs. It raised a question for procurement teams: could MPC or MPI become the solution to the protein craze?

For most, the answer was no. Customer specifications called for whey. And customers weren’t changing recipes.

October: No signs of cooling

Whey proteins became the exception in a weakening dairy complex.

Every other commodity was struggling. Whey kept climbing.

Demand continued its upward march across demographics and geographies. Western markets were far from peak per capita consumption. Developing regions had room for growth.

Here’s the kicker: retail prices for whey-containing consumer products hadn’t increased much.

No demand destruction. That was supposed to be the governor on price. Higher prices should trigger lower volume.

Instead, producers had sold through Q4 volumes. Now they were negotiating Q1 pricing with their customers. FOMO buying was real. Everyone wanted to lock in supply before prices went higher.

November: Parity with Europe

US WPI crossed parity with European prices.

Earlier in the year, US WPI traded $1.80/lb below Europe. It was the discount play. European customers who wanted cheaper supply bought US.

By November, that spread was gone. US prices had climbed. European prices had held steady.

US WPC80 gained $1/lb in two months while European prices sat flat.

The crossover was imminent. US WPC80 was about to trade above European levels for the first time.

The driver: demand rising while temporary US factory outages pinched supply.

High-protein exports were up 10.50% year-to-date through July. Japan had overtaken China as the top destination for US whey proteins.

December: Extraordinarily tight

December brought the market to a breaking point.

WPC80 markets showed signs of nothing. Not cooling. Not slowing. Not stabilizing.

“WPC80 extraordinarily tight,” traders reported. Buyers were “grateful to secure product at all.”

Colleagues who’d been away from the market came back to price quotes and didn’t believe them. They’d left a market at $8/lb. Now it was $11/lb. They thought they were reading the numbers wrong.

Jasper’s year-end report summed it up: “WPC80 markets show no signs of cooling. GLP-1-driven demand ever-increasing. Production capacity unable to expand quickly enough.”

WPC80 regular benchmarks got added to Vesper alongside instant. The market had grown big enough to track both grades.

High-protein dairy demand surged globally. Woolworths reported double-digit growth in high-protein categories. Chobani’s Fit line was up 50% year-over-year. Bega expanded from Australia into high-protein milk.

The consumer wasn’t stopping. Production capacity was the bottleneck.

The year in numbers

Let’s zoom out.

WPI trajectory: $6.70/lb (January 2024) to $10.50/lb (September 2025). That’s a 57% increase in 20 months. The market broke the $10/lb ceiling that seemed unbreakable.

WPC80 trajectory: Peak-to-peak, it hit all-time highs in December. Previous records set in 2011-2012 got broken by mid-year and stayed broken.

EU-US spreads: WPI premium blew out to $1.83/lb (4x average). WPC80 premium hit $1.58/lb (4x average). Both came partially back down by year-end but stayed 4x historical levels.

China rebalance: From 67 million pounds of rejected US supply, the market found homes. Japan became the outlet. EU supply got re-routed. US domestic demand absorbed the gap.

Production response: Manufacturers sprinted toward the highest-value proteins (WPI). Lower-value proteins (dry whey, permeate) got left behind.

Demand trajectory: Every consumer metric climbed. GLP-1 adoption. Per capita protein consumption in developed markets. High-protein product innovation. None of it let up.

The spread that opened: Milk proteins (MPI, MPC) stayed flat while whey proteins soared. That 4-6 year historical gap became a chasm. Procurement teams noticed. But switching costs meant they had to pay the whey premium anyway.

What this means for procurement teams

The US whey market in 2025 teaches a hard lesson about commodity dynamics.

Price doesn’t reflect scarcity alone. It reflects structural demand meeting constrained supply. When demand is inelastic (like GLP-1 creating a new normal for protein), prices move into uncharted territory. When substitutes carry switching costs, competitors can’t steal volume even at 50% premiums.

Tariffs have disproportionate impact on tight markets. US tariffs on China reached 145%. China’s retaliation hit 84% on US products. But tariffs didn’t move prices proportionally. They rerouted supply chains. They opened arbitrage. They created 4x historical spreads. The absolute dollar impact on a tight market is bigger than the tariff rate suggests.

Certainty is worth money. By November, having secured Q1 supply was worth $1+/lb of premium. Buyers locked in. They didn’t negotiate lower prices. They negotiated supply guarantees.

New product categories can absorb price pressure. WPI went from 30% of Vesper’s whey tracking to 40%+. It moved from specialty to mainstream. That created new volume channels even as prices climbed.

Production capacity is the real constraint. You can raise prices. You can expand demand. You can reroute supply. But you can’t instantly build new evaporation lines. Producers hit capacity. That ceiling became the price ceiling.

Expensive whey beats no whey. That was the lesson from 2025.

What’s next for US whey proteins?

The US whey protein market moves fast. Every week, new production data, trade flows, tariff developments, and demand signals reshape the picture.

Our US Weekly covers all of it: whey proteins, cheese, butter, NFDM, milk production, tariffs, and the global forces pulling US dairy prices in every direction. Written by Vesper’s dairy team, delivered to your inbox every Friday.