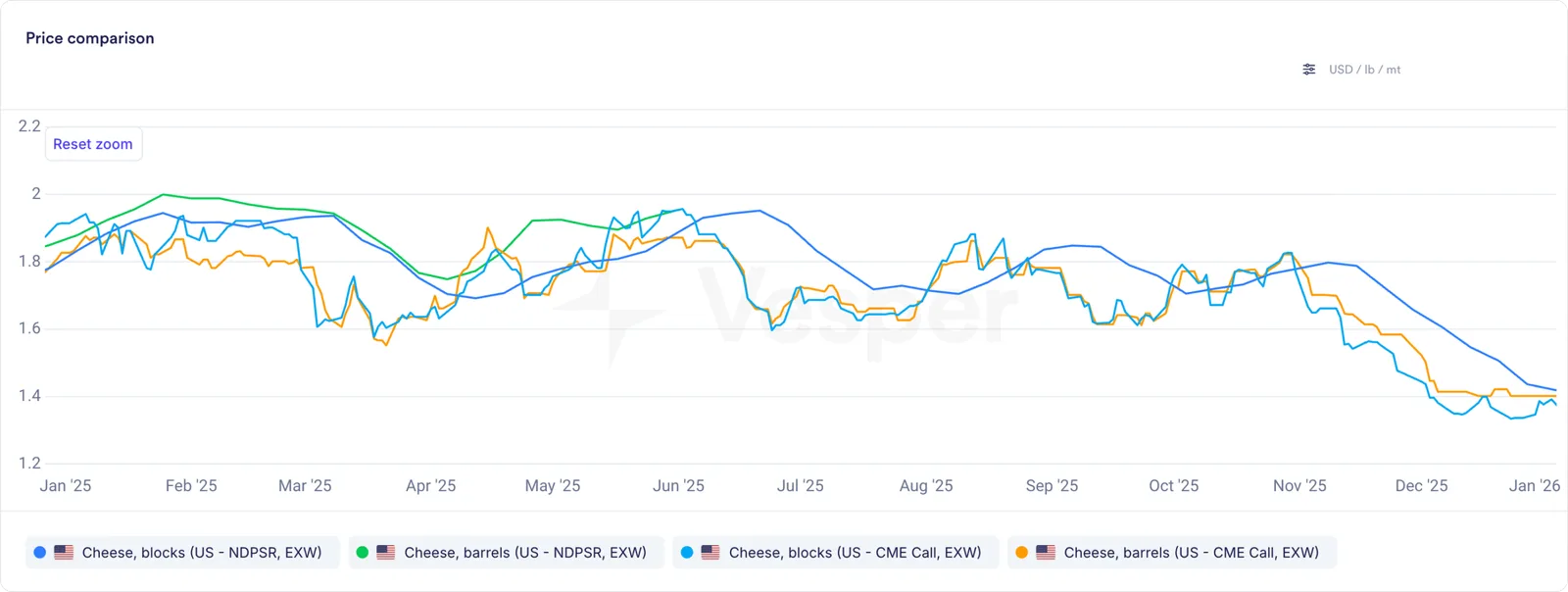

2025 was the year the US cheese industry hit a ceiling. New production facilities came online. Milk flowed in abundance. But domestic consumption stayed flat, and European price wars eroded the export advantage that had propped up margins for months. Prices fell 27% over the year, from nearly $2/lb to $1.47/lb.

US Cheese blocks and barrels prices according to NDPSR and CME Call in USD/lb

The January pricing surge, the May demand spike, the September collapse, the December floor at $1.47/lb. Each inflection point forced procurement teams to make decisions with incomplete information.

This is the month-by-month anatomy of what happened.

January: Factory restart, Prices climb

The year opened with a familiar pattern: holiday factory downtime creates a production dip, milk diverts to cheese, and prices tick up on lower supply.

CME cheese futures rose steadily in January. The CME Block market moved higher as processors worked through post-holiday scheduling. Cold storage data showed American cheese stocks down 7% year-over-year, a sign of tighter market conditions.

But the real signal was directional. Producers expected a slowdown in demand. They got the opposite. Cheese prices rose. Whey prices stayed favorable. The combination meant processors saw room to run, and new cheese capacity projects already approved began their final planning phase.

Key number: American cheese stocks down 7% YoY.

February: The bear case emerges

By mid-February, the CME futures curve flipped. Cheese prices flattened and began to feel real pressure.

This was the first signal that something had shifted. The bear case wasn’t new. Processors had been discussing new mozzarella capacity for months. But February was when traders started pricing it in.

Cold storage data confirmed the worry: American cheese stocks had only contracted 7% year-over-year, which meant that on an absolute basis, there was still plenty of inventory. And mozzarella was trading cheaper than cheddar, signaling that some of the new capacity was already producing.

New capacity was coming online faster than expected. Prices wouldn’t hold.

March: The floor collapses

March answered that question with brutal clarity.

CME Block cheese dropped $0.25/lb in a matter of days. That’s a 13% one-week decline. Processors watched their forward margins evaporate. The market wasn’t signaling a gradual softening. It was a waterfall.

Cold storage data showed American cheese stocks up 1% month-over-month, but down 7% year-over-year. Translation: production was starting to exceed the expected seasonal pattern. New mozzarella capacity was running. Cheddar faced headwinds.

Trade tariff headlines added uncertainty around key export markets.

March was when producers learned that new capacity plus slowing domestic consumption equals a market problem.

The pivot: Supply surged. Demand stayed flat. Prices paid the price.

April: Capacity, Not consumption

February cheese production data (released in April) showed the scale of what was happening:

• Mozzarella production: up 3.59% year-over-year

• Cheddar production: down 1.35% year-over-year

• Total cheese production: up 0.78%

The mix mattered. Mozzarella, the high-volume commodity cheese for pizza chains and foodservice, was growing. Cheddar, the higher-margin consumer favorite, was shrinking.

At the same time, milk production hit its strongest levels in years. The biggest dairy herds since May 2023 were pouring milk into the system. Some of it flowed to cheese. Some to whey powder. All of it meant supply would keep growing regardless of price.

Tariff uncertainty from “Liberation Day” political headlines added another layer of risk to export planning.

April was the month the industry acknowledged a simple fact: capacity expansion was no longer the upside story. It was the constraint.

Production reality: April set cheese facility highs. March had given a glimpse of what full capacity looked like.

May: The demand anomaly

Then something unexpected happened.

Cheese demand surged. Prices approached $2/lb.

US cheese consumption per capita had grown 11.28% over the past decade. That long-term trend wasn’t gone. US-China tariff negotiations and Indonesia trade agreements added to the optimism.

March cheese production (released in May) showed the real recovery: up 1.35% year-over-year, and cheddar roared back with +9.64% growth.

The narrative flipped. Sellers who had panicked in March suddenly saw a path back to margin. Prices approached $2/lb.

June: Post-spike reality check

Summer heat brought cooling. Prices fell from $2/lb back to $1.7/lb.

April cheese production came in at record highs: up 3.08% year-over-year. Translation: when you run new capacity at full tilt, you get a lot of cheese. The market had priced in the hope of tight supply. The data delivered the opposite.

But processors didn’t panic this time. Here’s why:

Weak US dollar meant US cheese was cheap on world markets. Exports surged. Japan and South Korea were buying. The export channel, which had looked uncertain in April, suddenly looked like the escape valve.

June was the month export strategy shifted from “nice to have” to “necessary.”

June reality: April highs turned into June oversupply. Exports became essential.

July: Exports stabilize, Prices steady

CME cheese held steady around $1.6/lb in active trading. This is where supply and demand met.

The production numbers were staggering. American cheese production was up 5.55% year-over-year. Cheddar had recovered fully, up 9.64%. But exports had already climbed to record levels.

“Liberation Day” financial market recovery in early July boosted overall commodity sentiment. Cheese exports hit record levels in May alone, with Japan and South Korea leading volume gains.

The market had found an equilibrium: record supply met by record exports, with prices depressed but stable.

Equilibrium price: $1.6/lb, sustained by export volume.

August: The shift to export business

A technical summer report changed the framing entirely.

Mozzarella hit 403.6M lbs in June. The CME was now carrying serious mozzarella contracts. What was once a captive domestic ingredient had become a traded commodity.

The narrative switched from “US market management” to “global competition.” H1 cheese production was well ahead of prior year. New facilities were running. Traders started watching European pricing more closely. The competitive dynamic was shifting.

Mozzarella scale: 403.6M lbs in a single month. Now a global pricing factor.

September: Competition deepens the fall

The price decline picked up speed in September.

Cheese production capacity expansions were completing their ramp. US cheese exports were strong: up 13.64% year-to-date (+92M lbs more than 2024). But competition had intensified.

• EU cheese production was ramping

• New Zealand was competitive

• US exports were strong in volume, not price

The data showed the split:

• US cheese exports: up 13.64% YTD, +92M lbs

• Total cheese exports surged 29% (+11,818 MT) in July, with cheddar up 143%

• But: 30% year-over-year price decline accelerating

Processors faced a brutal choice: lower prices to keep volume, or hold prices and lose share. Most chose volume. Commodity cheese rarely tolerates margin defense when global competitors can undercut.

September signal: Exports were the volume story. But pricing was the real problem.

October: The data black box

October brought a government shutdown. NASS dairy production data went dark. No official statistics on milk production, cheese output, or cold storage.

This meant traders made decisions without real-time information. Rumors filled the gap.

What was visible: European mozzarella prices had crashed to $1.47/lb while US prices held at $1.81/lb. That 33.5 cent discount was a ticking bomb for US competitiveness.

South Korea, a key growth market, showed fresh cheese imports up 51% year-to-date. Was that volume coming from the US or from cheaper European alternatives?

October was the month uncertainty spiked. Without data, producers had to make H4 decisions based on incomplete information and worse, based on competitive pricing moving against them in real time.

European pressure: $1.47/lb in Europe vs $1.81/lb in the US. The margin window was closing.

November: The margin collapse

By November, European prices had fallen so far that the US competitive advantage had evaporated entirely.

CME Block cheese hit its lowest level of the year. Domestic consumption, which had spiked briefly in May, couldn’t absorb record production. Strong milk production continued. Fierce European competition was now the binding constraint on US pricing.

The export story, which had sustained margins from June through October, had unraveled. Yes, the US was exporting more cheese in volume. But the price per pound was under sustained pressure from global competition.

The production growth story had one month to tell: August cheese production showed growth slowing to +0.52% year-over-year, down from 2%+ growth in previous months. The brakes were being applied.

After months of strong export performance, European pricing was eroding the US competitive edge. Producers who had bet on sustained export demand faced a reality: volume doesn’t help if margins disappear.

November reality: 13.64% more cheese exported Jan-Jul. But European prices $500/mt cheaper, which meant lower revenue per unit in the second half.

December: The year’s low

Cheese blocks hit their lowest level of the year in December. CME settled at $1.47/lb, a 17-month low.

Mozzarella faced global competition from cheaper alternatives. Record production of high-volume commodity cheeses met domestic consumption that had plateaued. There was no shortage of cheese. There was a shortage of buyers willing to pay January prices.

Aging inventory was expensive. Cheese that had been produced in June and held into December faced carrying costs, spoilage risk, and the reality that waiting hadn’t improved prices.

The market had compressed. A processor who made the capital investment to add capacity in 2024 was now operating that equipment at lower margins than planned. The 27% year-over-year price decline wiped out expected returns.

Year-end marker: $1.47/lb, 17-month low.

The arc: Supply wins, Price loses

Here’s what happened in 2025:

1. Capacity came online. New mozzarella and cheddar facilities started production in Q1 and Q2.

2. Milk production boomed. The biggest herds since May 2023 poured milk into the system.

3. Domestic demand stayed flat. US cheese consumption per capita was up long-term, but annual growth was modest.

4. Exports became the escape valve. From June through October, export volume kept prices from collapsing completely.

5. Global competition caught up. European prices fell hard, and by November, the US export advantage was gone.

6. Prices compressed to their limits. December marked the year’s low, and the industry prepared for volatility to continue into 2026.

The lesson for procurement teams: new capacity doesn’t disappear. It keeps producing. When global competition can undercut, margins move fast. The January strategy of capturing supply advantage evaporated by December.

What’s next for US cheese?

The US cheese market moves fast. Every week, new production data, cold storage reports, export volumes, and competitive pricing shifts reshape the picture.

Our US Weekly covers all of it: cheese, butter, whey, NFDM, milk production, tariffs, and the global forces pulling US dairy prices in every direction. Written by Vesper’s dairy team, delivered to your inbox every Friday.