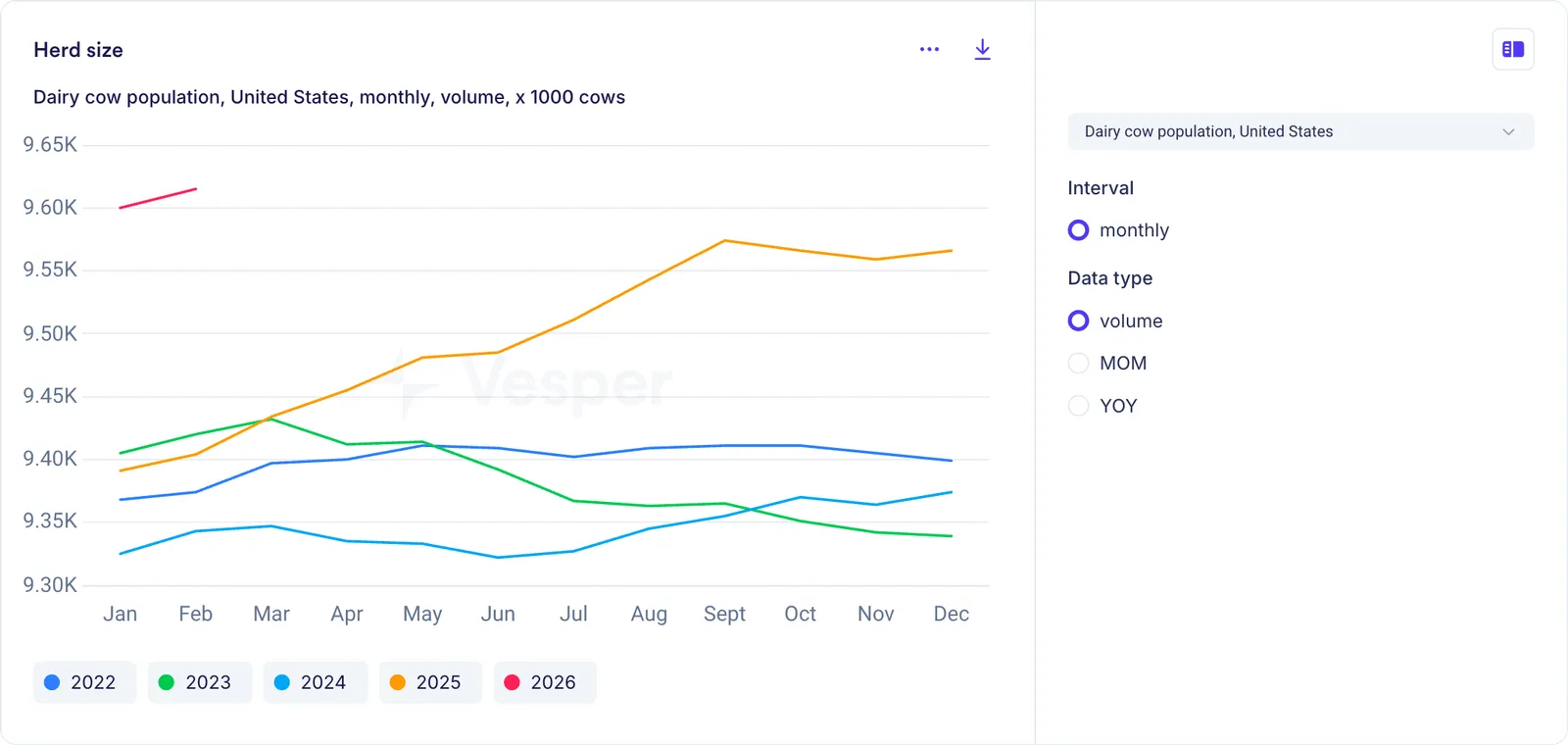

The US dairy herd reached 9.615 million cows in early 2026, the largest since 1993, with milk production up 3.2% year-over-year in January and every region showing growth. The supply picture looked comfortable.

US Dairy cow population over the past 5 years

Look behind the headline number and a different story emerges. Replacement heifer inventory dropped to a record low of 2.922 million head in October 2025, the heifer-to-cow ratio fell to 41.9 (the lowest since 1991), and heifer prices spiked 75% to $3,010 per head. The herd driving today’s record milk production is not being replaced at the rate needed to sustain it, and while today’s supply is strong, the pipeline behind it is thinner than anyone would like.

The explanation starts with a breeding decision: farmers chose beef-cross calves over dairy replacements because beef paid better, draining the heifer pipeline over several years. That left a large, productive herd with almost no bench behind it, vulnerable to any shift in margins that would trigger culling. And the timing couldn’t be worse, with over $10 billion in new processing capacity coming online that needs more milk, not less.

Why farmers chose beef calves over dairy replacements

The heifer shortage has a specific cause: economics. Beef-on-dairy breeding, the practice of mating dairy cows with beef bulls rather than dairy bulls, has become widespread because a beef-cross calf sells for significantly more than a dairy heifer calf at the same age, and when beef prices sit near historic highs, the incentive to breed for beef is powerful. Heifer inventory had fallen 18% since 2018 as farmers increasingly bred to beef sires for better returns, and the trend accelerated as beef values climbed through 2024 and 2025.

Gender-sorted semen, which allows farmers to choose the sex of calves and produce more females for dairy replacement, partially offset the trend with sales up 17.9%, but the adoption rate wasn’t fast enough to close the gap. Meanwhile, heifer prices themselves reflected the shortage: at $3,010 per head, up 75% from recent years, buying replacement heifers became a major capital expense, and farmers who wanted to expand or simply maintain their herds faced significantly higher costs to do so.

The path to this point follows a familiar dairy cycle. In 2022, margins compressed while beef prices climbed, and many farmers chose to sell cows to slaughter at historically high beef prices rather than keep them milking at thin margins. The herd shrank significantly through 2022 and into 2023. Then margins improved, milk prices rose, and farmers started rebuilding, pushing cow numbers from a trough to 9.575 million by the end of 2025 and 9.615 million by early 2026, up 204,000 head year-over-year. But the pipeline of young animals didn’t rebuild at the same pace, because farmers had been breeding for beef calves instead of dairy replacements throughout the recovery.

A large herd with a thin bench

By early 2026, the US dairy industry sat in a paradox. The herd was large with cow numbers at their highest in over 30 years, feed costs had dropped to decade lows, and the short-term economics of producing milk were favorable. But the cows driving this production were the ones already standing in barns, staying in the milking herd longer because it was profitable to keep them there. Culling rates were low and every cow that could produce was producing.

What wasn’t happening was a wave of replacement animals coming up behind them. The young stock pipeline was historically thin, and when those current cows eventually leave the herd, whether through age, health, or a future downturn in margins, replacing them will be slower and more expensive than it has been in decades. In early 2025, replacement heifer numbers had already hit a 47-year low at 3.914 million head, and by October 2025 they’d dropped further to the record low of 2.922 million. For every 100 cows currently milking, there were only about 42 heifers waiting in the pipeline.

Milk production growth in 2025 and early 2026 was a function of herd size plus yield per cow, and both were performing well. January 2026 came in at 19.81 billion pounds, up 3.21% year-over-year, February showed 2.87% growth with 15,000 new cow additions higher than expected, and the South posted the fastest relative growth at over 6%, more than double the national average. None of this signals an imminent problem. The concern is what happens next.

What happens when margins turn

The current situation works as long as dairy margins stay favorable enough to keep cows milking, but margins are not guaranteed. Beef prices remain near historic highs, and if dairy margins compress, the incentive to cull increases. When culling accelerates against a backdrop of record-low replacement inventory, the herd could shrink faster than it can be rebuilt.

This dynamic was already visible in late 2025 when October brought the first US dairy herd decline since December 2024, with the herd falling by 7,000 head as the combination of softening dairy commodity prices and persistently high beef prices made culling attractive again. A Wisconsin dairy farmer made headlines by proposing a deliberate cull of the US dairy herd to balance milk supply, with his math showing that a 1% surplus can crater milk prices by $3-5 per hundredweight. When farmers start talking about herd reduction as a market management tool, it tells you how tight margins have become.

Many farmers were already crossbreeding dairy cows with beef bulls to diversify income, which is a rational individual decision but at scale means fewer dairy heifers entering the system, compounding the replacement shortage. Recovery in heifer numbers wasn’t expected until after 2027, and the combination of beef-on-dairy breeding, high heifer prices, and low replacement ratios creates a scenario where the current production growth is being borrowed from the future.

$10 billion in new processing capacity needs more milk

The timing of the heifer shortage couldn’t be worse for the dairy processing industry. Over $10 billion had been invested in new US processing facilities scheduled to require milk through 2027 and 2028, with 53 new or expanded dairy factories in the pipeline. Bel Group committed $200 million to expand its Babybel plant in South Dakota and Schreiber Foods invested $133 million in Pennsylvania, just two examples from a single week in March 2026.

Every new cheese plant, expanded whey protein facility, and additional butter churn needs milk, and the processing industry was building capacity for growth while the cow population was structured for maintenance at best. If the herd contracts while new processing capacity comes online, competition for milk intensifies, plants that can’t secure milk supply face underutilization, farmers who do have cows gain pricing leverage, and the downstream effects ripple through every dairy commodity.

What this means for procurement teams

The herd replacement math matters for anyone buying dairy ingredients with a time horizon beyond the next quarter.

Current production data doesn’t tell you about future production capacity. The herd is large today, but the heifer-to-cow ratio says the industry’s ability to maintain this herd through the next downturn is weaker than at any point since 1991.

New processing capacity assumes milk availability. The $10 billion+ investment wave in US dairy processing is a bet on sustained or growing milk supply, and if that supply growth stalls because herd replacement can’t keep pace, competition for milk will intensify. Procurement teams who rely on specific plants or regions should understand their suppliers’ milk sourcing security.

Yield gains have limits. US dairy farmers have been exceptionally successful at breeding and feeding for both components and volume, with milkfat production up 4.33% year-to-date through November 2025, nearly two percentage points ahead of fluid milk growth. But yield per cow can’t increase indefinitely, and at some point cow numbers become the binding constraint. The heifer data suggests that point is approaching.

Beef economics are a leading indicator for dairy supply. When beef prices are high and dairy margins compress, cows get culled, and the current beef-on-dairy breeding trend means fewer replacement heifers are being born. Tracking beef markets isn’t a distraction for dairy procurement teams; it’s a forward indicator for milk supply.

The adjustment period will be measured in years, not months. A heifer born today doesn’t produce milk for roughly two years, and even if breeding patterns shifted immediately, the heifer pipeline wouldn’t normalize before 2028 or later. That’s a structural constraint, not a cyclical one.

What’s next for US milk production?

The US dairy production picture moves fast. Every month brings new data on herd size, milk output, component yields, and the economics that drive farmer decisions.

Our US Weekly covers all of it: milk production, cheese, butter, whey, NFDM, and the global forces pulling US dairy prices in every direction. Written by Vesper’s dairy team, delivered to your inbox every Friday.