The food industry has always evolved alongside shifts in consumer behaviour. Over the past decade, manufacturers have reformulated products in response to sugar reduction initiatives, plant-based preferences, clean-label expectations, and demand for healthier fat profiles. Each wave has required product developers and procurement teams to adapt ingredient strategies without compromising cost control.

GLP-1 medications appear to be shaping another such cycle.

Originally developed for diabetes management and now increasingly used for weight loss, these medications influence appetite and satiety. Users often consume smaller portions and report reduced cravings for calorie-dense foods, particularly those high in sugar. At the same time, healthcare professionals frequently emphasise the importance of maintaining adequate protein intake during weight loss to preserve lean muscle mass.

The result is not the disappearance of categories such as dairy beverages or breakfast cereals. Rather, it is a gradual adjustment in how those products are formulated. Sugar levels are reduced. Protein density is increased. Whole grains and fibre gain emphasis. Fat profiles are reconsidered.

From a formulation perspective, these shifts may appear incremental. From a cost perspective, they can be structural.

To better understand this impact, we built cost models for two categories: chocolate milk and granola, comparing traditional formulations with reformulated versions aligned with lower sugar, higher protein or improved fat positioning. We then applied pricing forecasts to examine how those changes affect procurement decisions.

Chocolate milk: when protein becomes the dominant cost driver

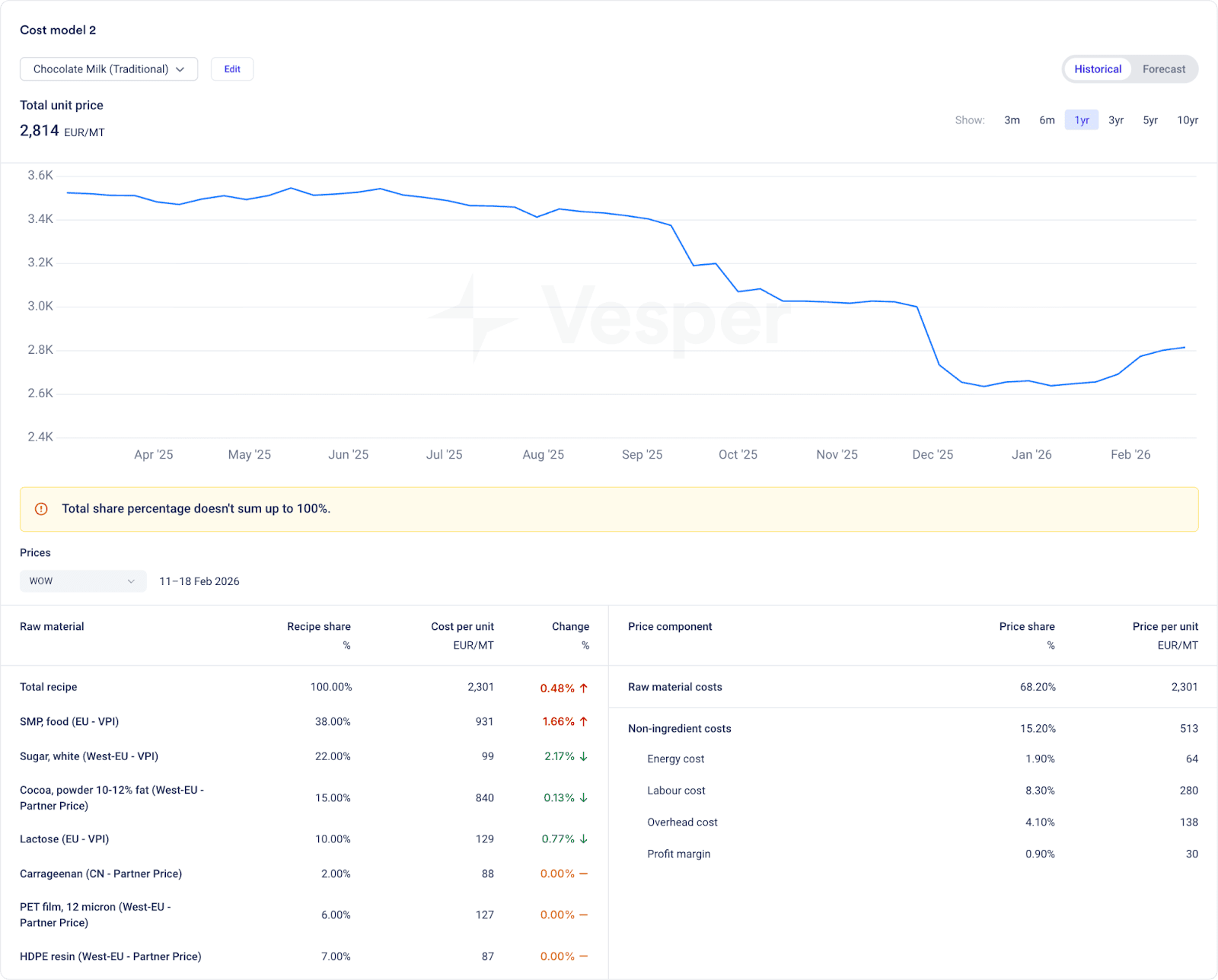

A traditional chocolate milk recipe is relatively straightforward. In our model, it consists primarily of skimmed milk powder, sugar, and cocoa, with stabilisers and packaging completing the structure. The total unit price comes to €2,801 per metric ton. Commodity exposure is distributed across dairy powders, sugar and cocoa markets, creating a relatively balanced cost base.

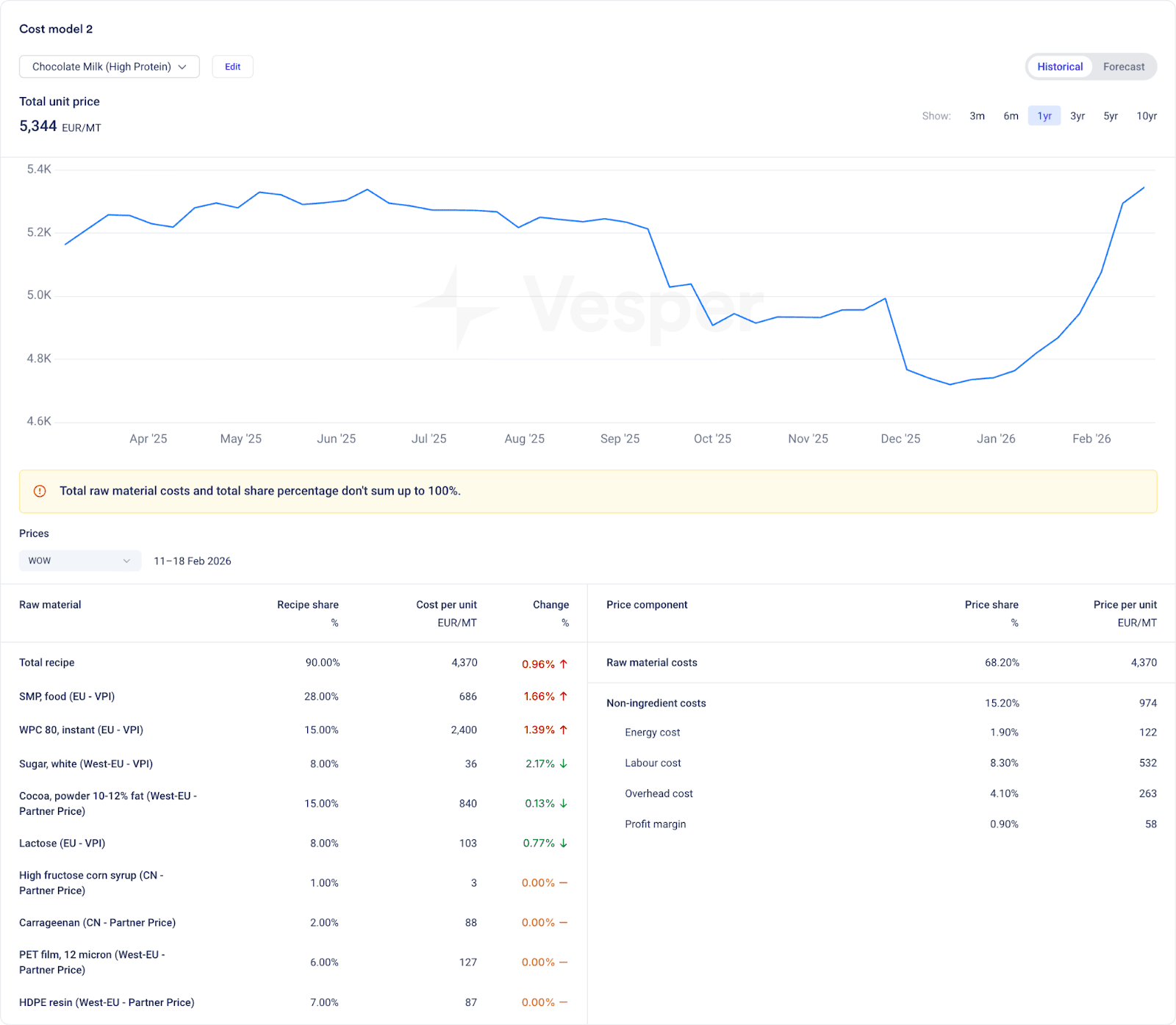

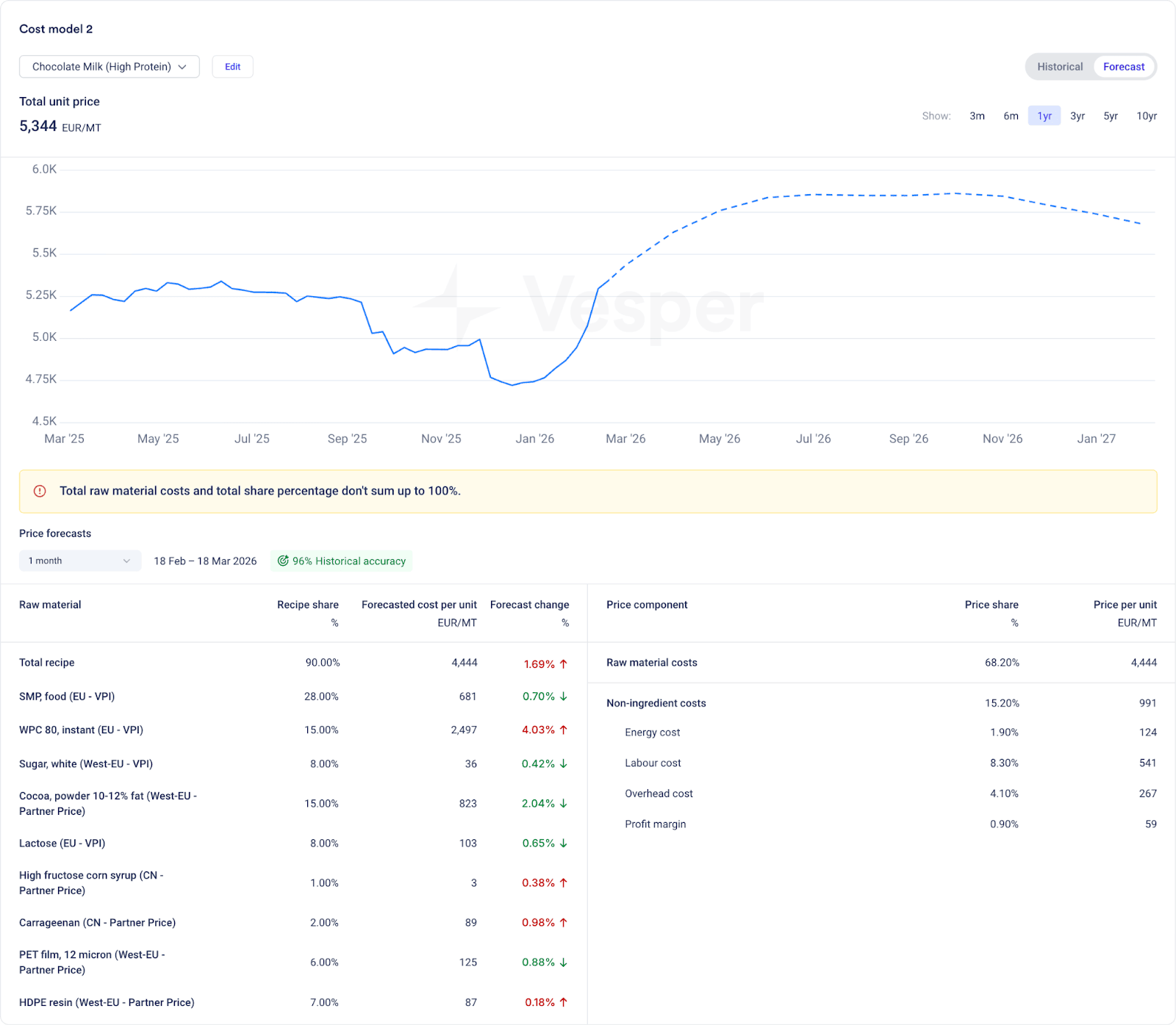

When the formulation is adjusted to reflect higher protein and lower sugar positioning, the structure changes significantly. Sugar is reduced from 22 percent to 8 percent, while whey protein concentrate (WPC80) is introduced at 15 percent inclusion. Skimmed milk powder is slightly reduced to accommodate the higher-value protein ingredient.

The total unit price increases to €5,344 per metric ton.

The driver of this increase is clear. Whey protein concentrate carries a materially higher price than sugar or standard milk solids. At 15 percent inclusion, it contributes approximately €2,400 per metric ton to the raw material base. What was once a relatively diversified cost structure becomes heavily influenced by protein markets.

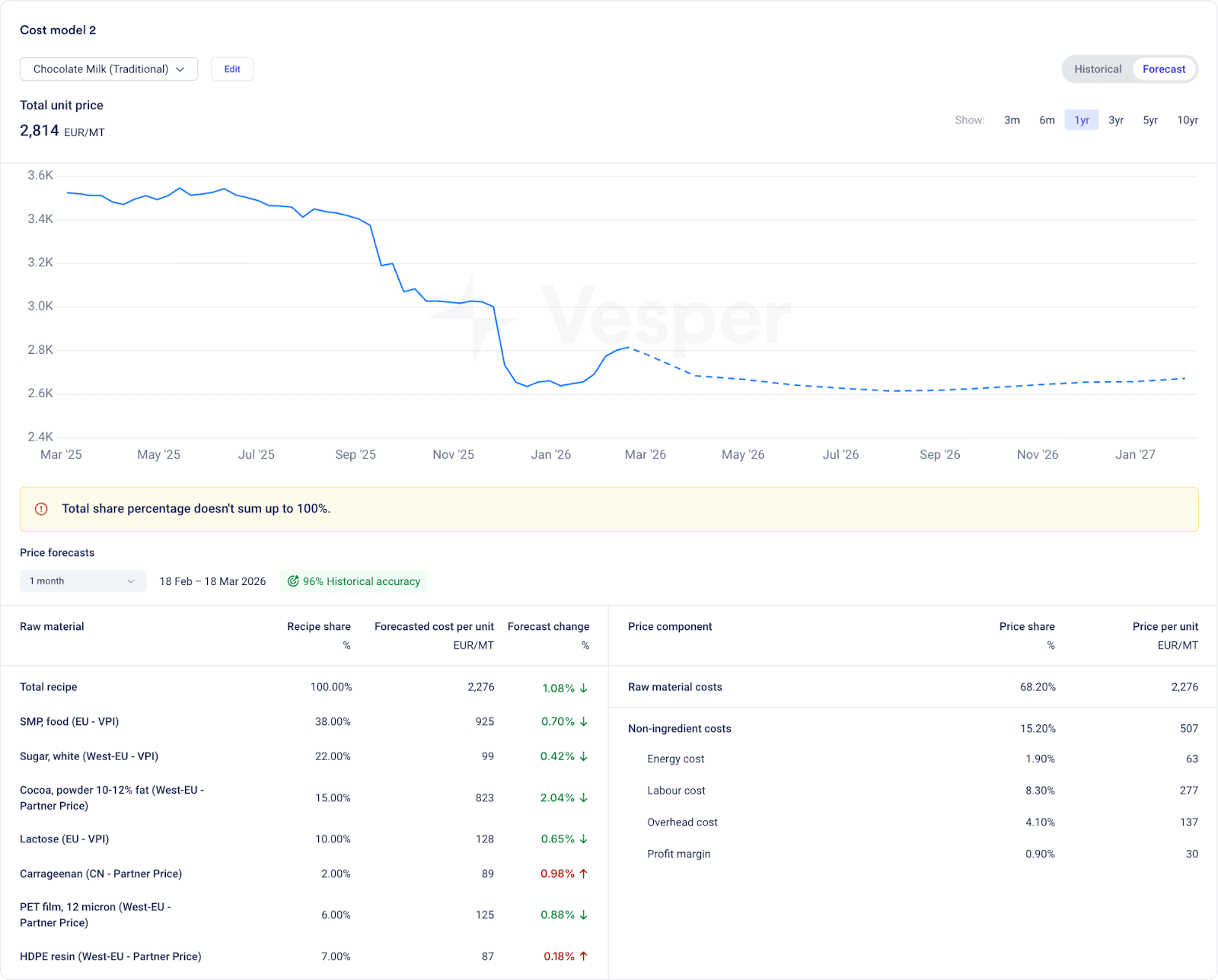

Extending the analysis with forward pricing adds further clarity. The forecast for the traditional chocolate milk model suggests moderate softening in skimmed milk powder and stable sugar pricing, resulting in a projected cost of €2,276 per metric ton. The reformulated version, however, remains sensitive to whey protein movements. With WPC80 forecasted to rise by just over 4 percent, the projected cost stands at €4,444 per metric ton.

Even small movements in protein pricing now have an outsized effect on overall cost.

For procurement teams, this shift is consequential. In the traditional model, exposure is spread across multiple markets. In the reformulated model, whey protein becomes a primary risk driver. Forward contracting decisions, supplier negotiations, and hedging strategies must adapt accordingly. Reformulation transforms not just the nutrition panel, but the volatility profile of the product.

Granola: sugar reduction and oil optimisation

Reformulation linked to GLP-1 trends is not limited to protein. Reduced sugar and improved fat positioning are equally relevant.

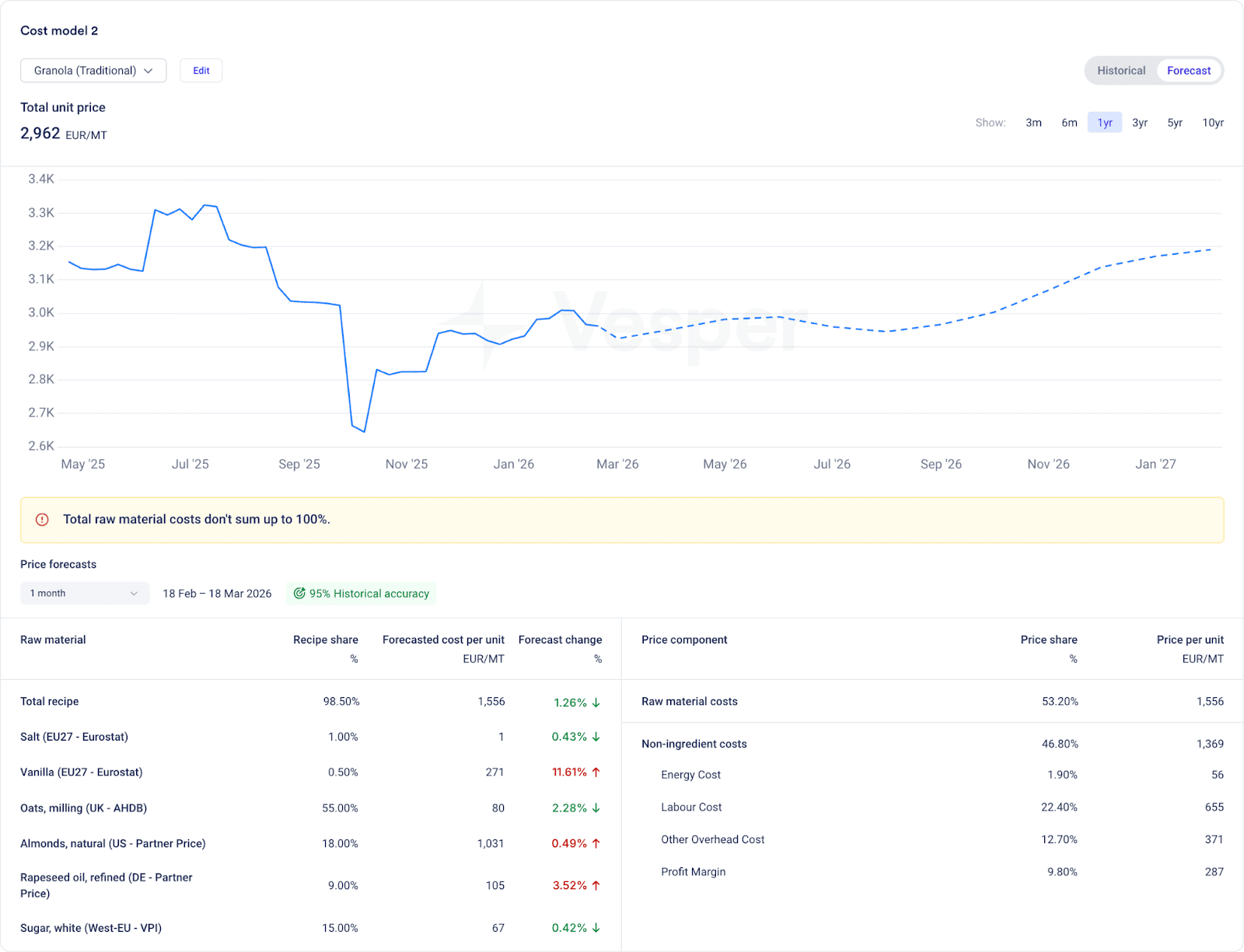

The traditional granola model consists of oats, almonds, sugar and rapeseed oil. At €2,864 per metric ton, its cost structure reflects exposure to grain markets, nut markets, sugar and vegetable oils. The profile is diversified, with no single ingredient overwhelmingly dominating cost.

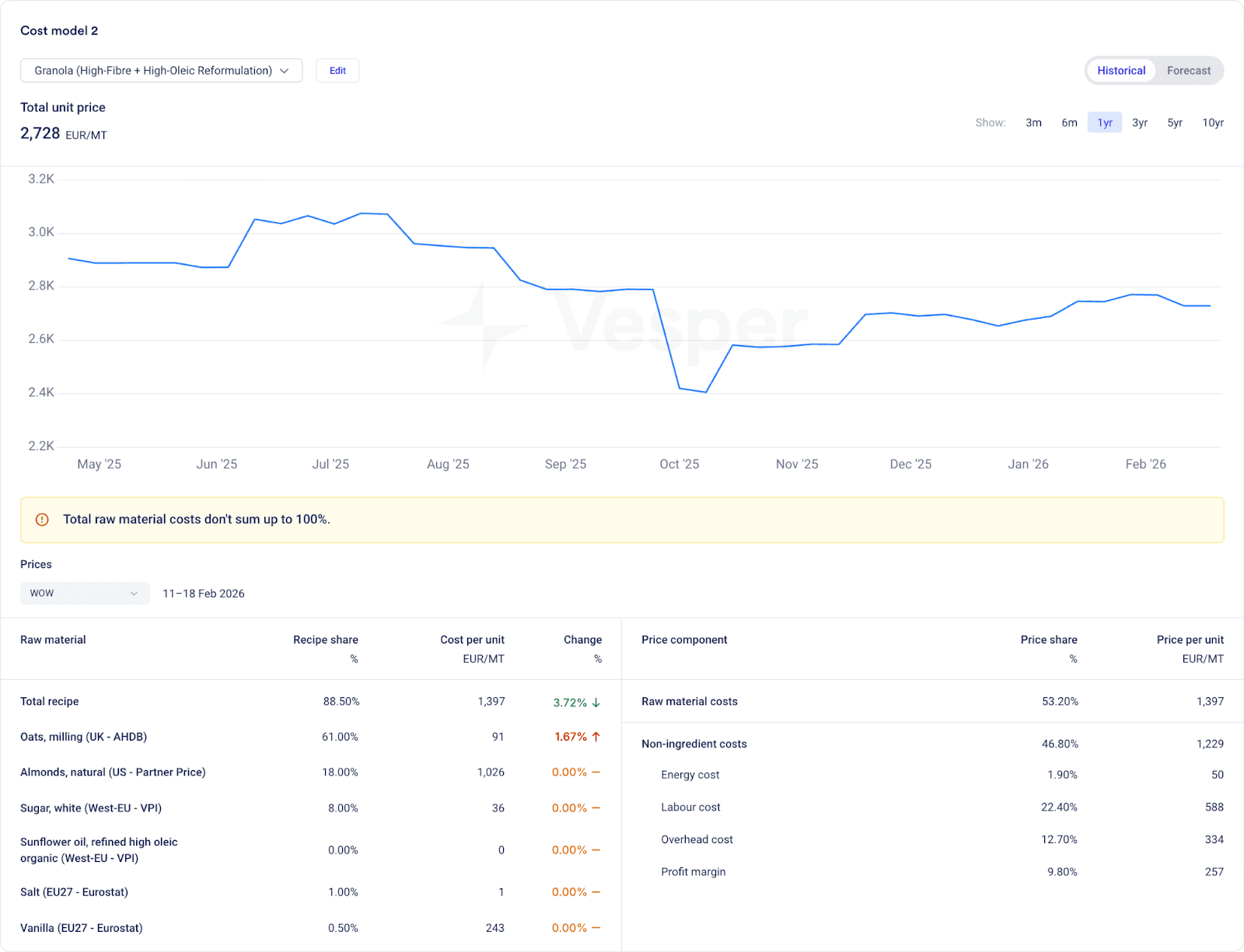

In the reformulated version, sugar is reduced from 15 percent to 8 percent and oats are increased from 55 percent to 61 percent, supporting higher whole-grain positioning. Rapeseed oil is replaced with high-oleic sunflower oil, a shift that aligns with ongoing efforts to optimise fat composition and oxidative stability.

High-oleic sunflower oil offers higher monounsaturated fat levels and improved resistance to oxidation, which can support longer shelf life and premium health positioning. While rapeseed oil is already considered a balanced fat source, manufacturers often make such adjustments to align with specific nutritional narratives and performance characteristics.

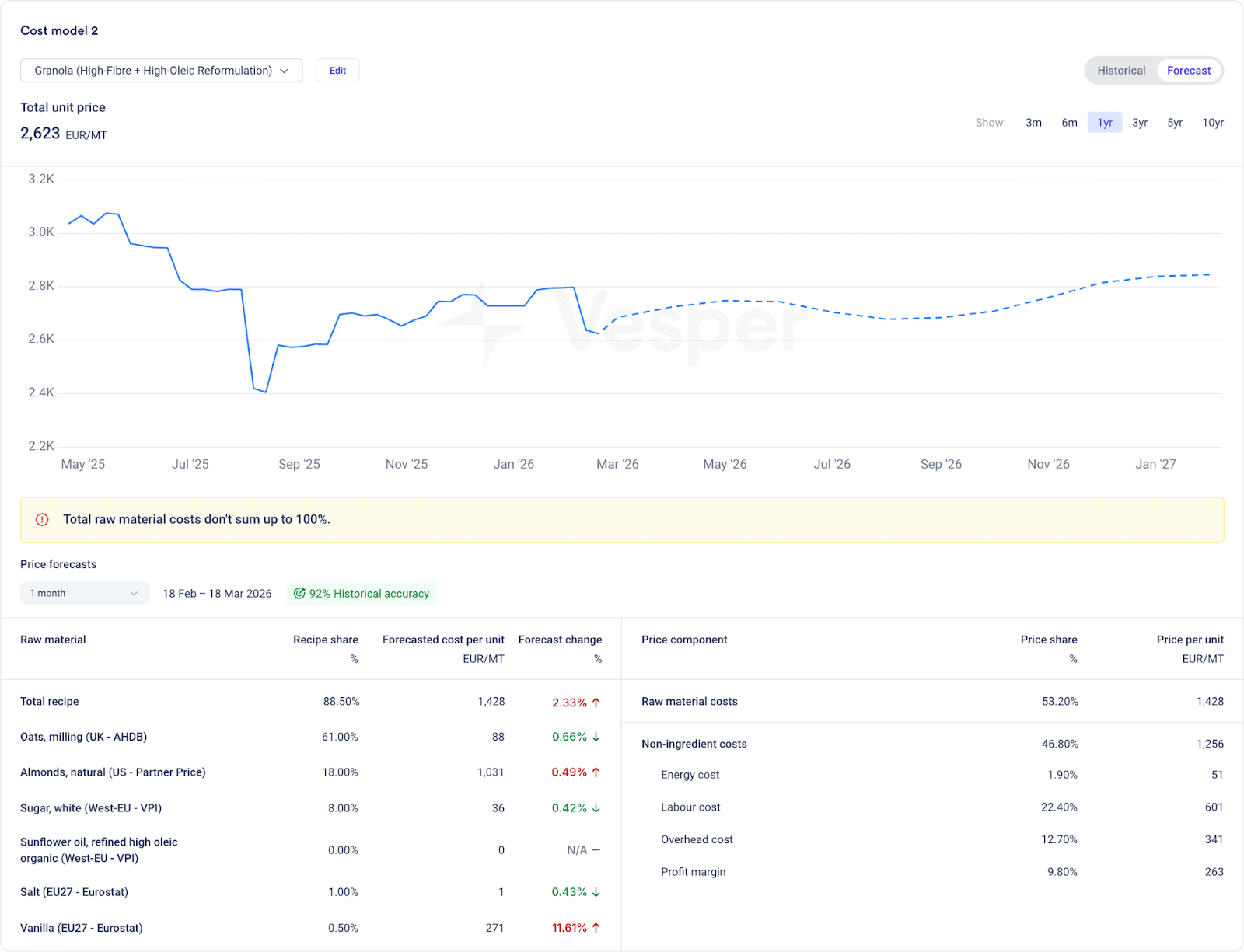

The reformulated granola model comes in slightly lower at €2,728 per metric ton.

However, the more meaningful change lies in exposure redistribution. Sugar sensitivity declines. Grain exposure increases. Oil exposure shifts from rapeseed markets to sunflower markets.

When forward forecasts are applied, both versions show moderate upward pressure, driven by almond and flavour components. Yet the reformulated version now requires closer monitoring of sunflower oil markets rather than rapeseed. Supplier relationships and hedging considerations evolve accordingly.

Reformulation as a procurement decision

Across both examples, a common pattern emerges. Reformulation rarely eliminates cost. Instead, it redistributes it.

In chocolate milk, cost concentration shifts toward whey protein. In granola, exposure shifts away from sugar and toward grains and sunflower oil. Total cost may rise, fall or remain stable, but the underlying sensitivity changes.

For procurement teams, this means that formulation decisions must be evaluated through a financial lens. Ingredient adjustments influence:

- Commodity dependency

- Volatility sensitivity

- Forward contracting priorities

- Supplier diversification strategies

Cost models provide the framework to quantify these shifts before products reach scale.

By connecting ingredient costs with non-ingredient costs, such as packaging and processing, it allows manufacturers to see the full unit economics of a product, not just raw material exposure.

By linking ingredient inclusion rates with real-time pricing and forward forecasts, they allow teams to simulate scenarios and understand margin risk under different market conditions, similar to how we demonstrated in our breakdown of chocolate bar manufacturing costs.

A structural but familiar cycle

GLP-1-driven reformulation is not unprecedented. It follows the same structural logic as previous industry shifts. Consumer behaviour evolves, product composition adapts, and procurement strategies follow.

What distinguishes this cycle is the degree to which protein and specialised ingredients can concentrate cost exposure. As manufacturers increase protein density or adjust fat profiles, they may inadvertently increase sensitivity to specific commodity markets.

Understanding that connection is essential.

Reformulation is often viewed as a product development exercise. In practice, it is equally a financial strategy decision. And in an environment characterised by commodity volatility, visibility into cost exposure is no longer optional.

It is foundational to protecting margins.

If you’re evaluating reformulation scenarios, start by modelling your current recipe structure and comparing it to alternative ingredient compositions. Our step-by-step guide explains how to structure your first cost model and integrate forward commodity forecasts into your analysis.