Skim milk powder is one of the most widely traded dairy ingredients in the world. It is the dehydrated form of skimmed cow’s milk and a long-life building block that ends up in infant formula, recombined drinking milk, bakery, confectionery, sports nutrition, and ice cream. Most of it crosses a border at some point between the dairy plant and the finished product, which is why a single specification difference can decide where it sells, who buys it, and at what price.

The United States is one of the larger producers. US dairy plants in California, Idaho, and the Upper Midwest ship a meaningful volume into global export tenders every week. Until recently, the price they ship at was difficult to read from outside the trade, because of a quiet split inside the product itself: there are actually two skim milk powder specifications, and only one of them had a public US price benchmark.

This article explains the split, walks through the public price reporting that existed before, and shows how Vesper closed the gap with the new US SMP price benchmark; built using the same Vesper Price Index methodology we use across categories where public reporting falls short.

NFDM and SMP: two specifications for the same product

The two specifications are NFDM and SMP.

NFDM stands for Nonfat Dry Milk. It is the US-standard skim milk powder, defined under US dairy standards and used as the reference product in domestic trade and in some export trade. It is what plants sell into the US bakery, confectionery, and ingredient markets, and what gets reported through US government and exchange channels.

SMP stands for Skim Milk Powder. It is the international standard, defined under Codex Alimentarius and the European Union’s dairy regulations. It is the reference product in most non-US trade, and the specification most international buyers (including buyers in Europe, North Africa, the Middle East, and Southeast Asia) write into their contracts.

The two products are similar enough to compete in the same global tenders. They are not similar enough to be interchangeable in a contract. Our data analyst Jasper put it cleanly in an internal note last month:

“NFDM and SMP look like the same product on a shelf, but they are written into different specifications. SMP carries a minimum protein content of 34% under Codex and EU standards, with defined heat treatment classes. NFDM is governed by US standards that do not impose the same minimum protein floor and use a different vocabulary for heat treatment. The two products overlap heavily in practice, but a contract written for SMP is not the same instrument as a contract written for NFDM. The minor variations in composition, in heat class language, and in tested parameters are exactly the kind of detail a global buyer pays attention to when sourcing from multiple regions.”

The contract specification and the indexed price need to match. A buyer writing a contract for SMP delivered into Algeria, with a defined protein floor and a defined heat class, cannot reference a US NFDM price as the settlement instrument and have it hold up in a tender process or an audit.

What public price reporting exists for NFDM

NFDM, the US-standard product, has several public price references. Each one is published by a different body, on a different schedule, for a different audience.

The CME spot call is a daily exchange settlement on NFDM. Buyers and sellers transact small lots in a structured trading session each morning, and the resulting settlement price is published by the exchange.

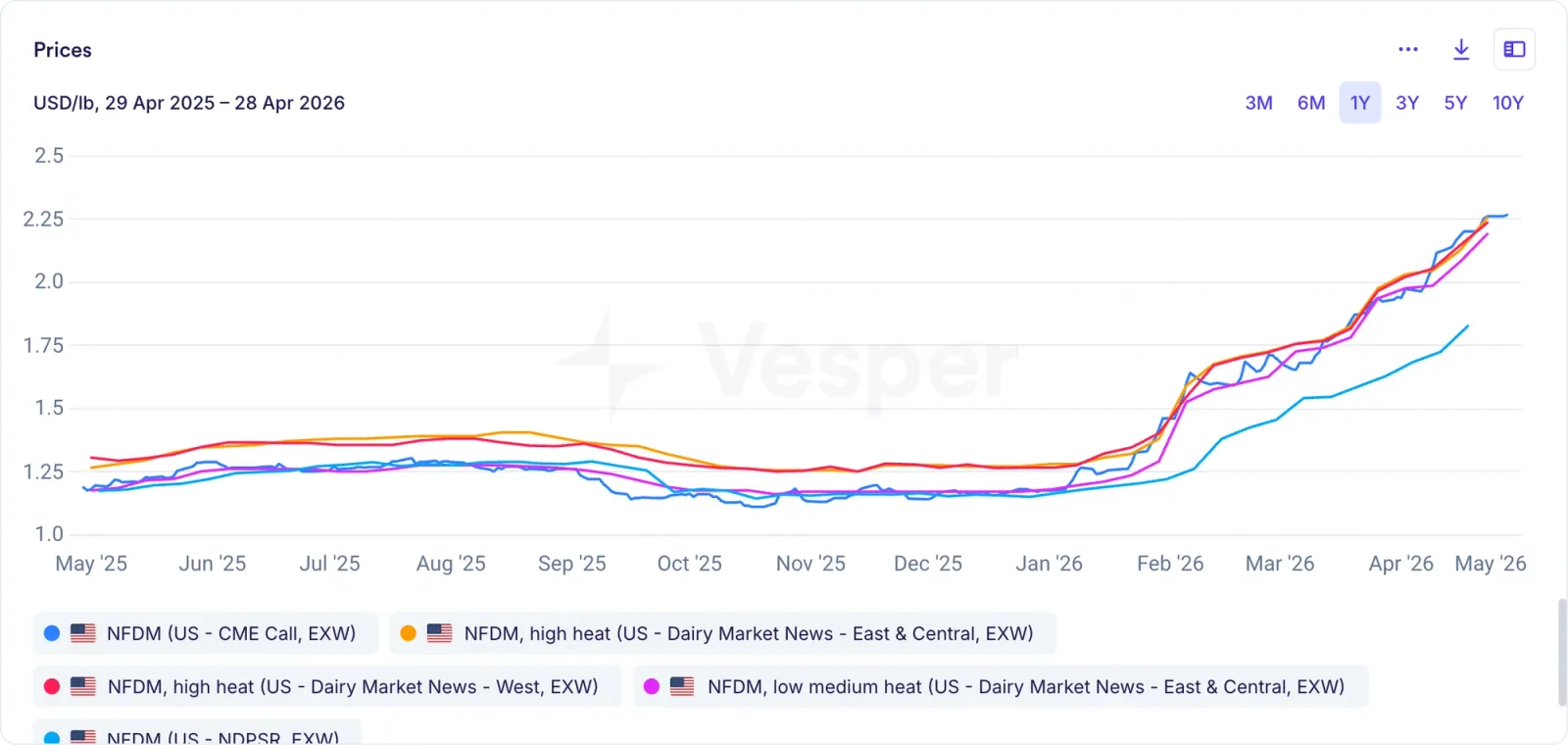

USDA Dairy Market News publishes regional weekly assessments of NFDM, split by heat treatment class. The two main splits are NFDM high heat (covering the West, East, and Central regions) and NFDM low medium heat (covering the East and Central regions).

The NDPSR survey, run by USDA, publishes a national weekly price for NFDM based on mandatory plant-level reporting. The NDPSR price is the input that USDA uses to calculate the Federal Milk Marketing Order Class IV price.

Vesper carries all of these on the platform, plus a forecast on each.

Vesper US NFDM price coverage across NDPSR, CME spot call, and Dairy Market News regional assessments

The gap on the SMP side

Public price reporting for the United States has historically focused on NFDM. SMP-specification production from US plants has not had an equivalent published reference, even though the volume going into export tenders is significant.

The reason is partly structural. NFDM is what US plants sell domestically and what the US regulatory framework reports against, so the public infrastructure (the CME, USDA Dairy Market News, NDPSR) reports NFDM. SMP, the international specification, is something US plants produce primarily for export, and the trade has historically settled in private invoices and broker conversations rather than in any public survey.

For a global buyer trying to compare US-origin SMP against European SMP and Oceania SMP in a tender process, this left a hole. There were public references for the European and Oceania prices. There was no public reference for the US price on the same specification.

The new Vesper US SMP price benchmark

We built a separate VPI panel for US-origin SMP, with its own buyer-side and seller-side submissions, its own validation against the EU and Oceania SMP references, and its own weekly publication schedule. The benchmark sits next to the NFDM coverage on the platform and reflects the price US plants are actually exporting at on SMP specifications.

The decision to publish two distinct US prices, one for NFDM and one for SMP, came from the same place as the rest of the methodology: the contract specifications are different, so the prices have to be different. Treating US SMP as “NFDM with a basis adjustment” would have flattened the distinction at exactly the moment a buyer is trying to manage it.

How the Vesper Price Index is built

The Vesper Price Index, or VPI, is the methodology behind the new US SMP price and the rest of Vesper’s proprietary benchmarks. It is what we use across commodity categories where public data is missing, fragmented, or does not match how buyers actually transact. The methodology rests on three elements.

Direct trade collection sits at the centre. We collect transacted prices from buyers, sellers, and traders inside each category, weekly, on a confidential basis. Each submission is a real deal at a real specification, not a quote or a desk estimate. The buyer-side and seller-side submissions cross-check each other and surface inconsistencies before the index is calculated.

Validation against available public references comes next. Where a public benchmark exists for a similar product (an NFDM print, a European SMP listing, an Oceania GDT result), the VPI is read against it for plausibility. Drift between the VPI and the public references is investigated rather than averaged away.

Publication on a fixed weekly schedule completes the loop. Each VPI is published on a defined day with a documented panel and an audit trail back to the underlying methodology. A buyer who references the VPI in a contract knows exactly what the panel covered, when it published, and how the price was derived.

The methodology produces a benchmark designed to hold up in front of finance, in front of an auditor, and across the table from a counterparty using a different reference.

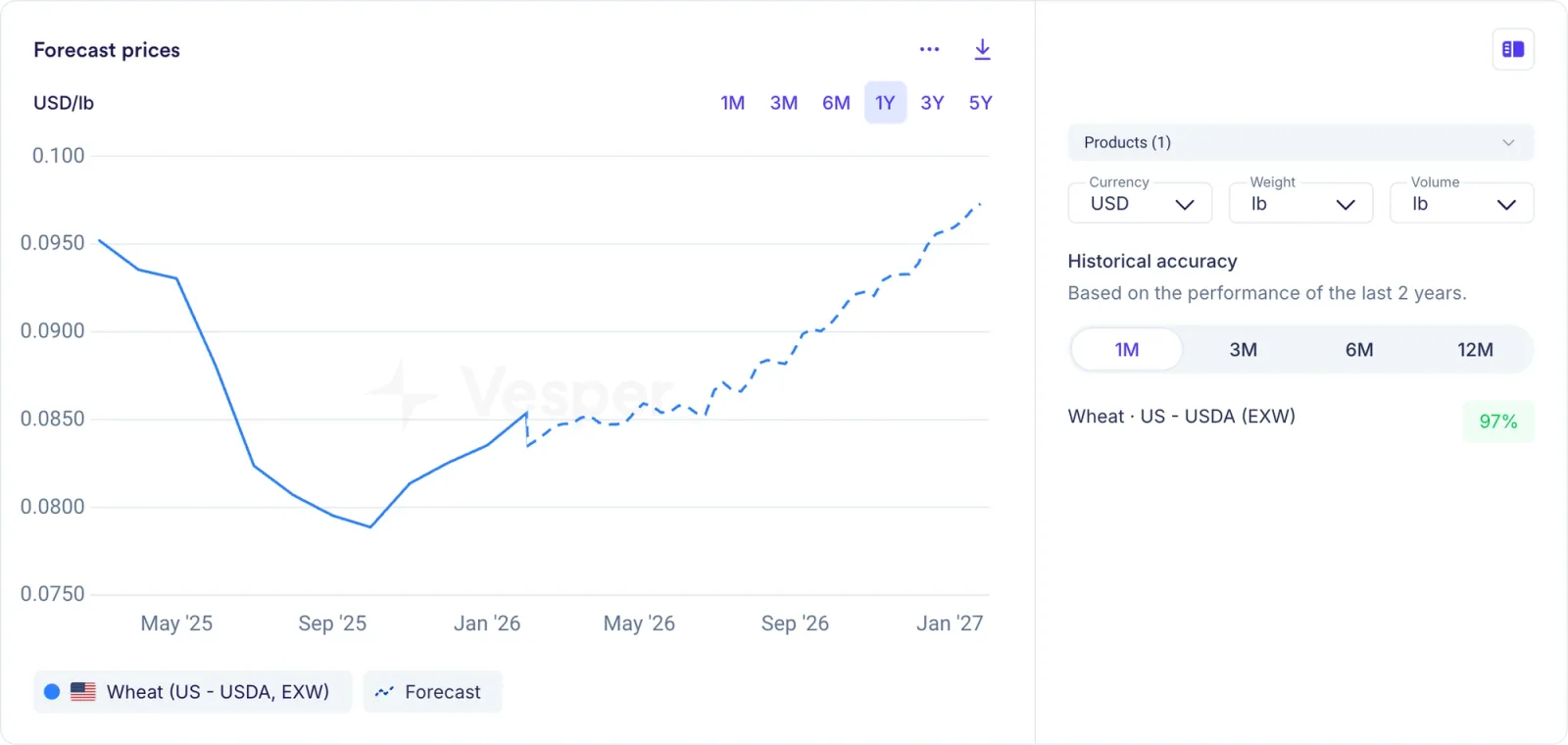

Forecasts on every NFDM and SMP series, side by side

Every NFDM and SMP price Vesper carries has its own forecast attached. The forecast layer is the second half of the workflow: a buyer reads the historical price to understand where the market has been, and the forecast to make a defensible decision about where it is going.

For SMP specifically, that means three regional forecasts can be read against each other on a single chart.

Vesper SMP forecasts for the EU (96% at 1M), Oceania (95% at 1M), and US (96% at 1M) VPIs, plotted together with one-year forward paths

The chart above is the three SMP VPIs Vesper publishes (European, Oceania, and the new US benchmark) plotted on the same axis in USD per pound, from May 2025 forward. Solid lines are the historical prices and dashed lines are the forecasts. Historical accuracy at the one-month horizon sits at 96% for EU SMP, 95% for Oceania SMP, and 96% for US SMP, measured over the last two years.

For a global buyer, this is the picture that did not exist before. The basis between the three origins is now visible at a glance: when the US line drops below the EU line, US-origin SMP is competitive into export tenders against European product; when the Oceania line moves higher than the others, that origin is pricing out of certain destinations. The forward paths extend the same comparison out a year, on the same specification, in the same units.

The same principle applies on the NFDM side. NDPSR has a Vesper forecast that procurement and finance teams use to anticipate where the next FMMO Class IV price is likely to settle. CME spot call has its own forecast running on the same chart as the historical print. The Dairy Market News regional series, both the high heat and low medium heat splits, each have a dedicated forecast. A buyer indexed against NFDM high heat West Coast reads a forecast on that specific series, not on the national average.

The full coverage today, both historical and forward, includes:

- NDPSR (the national weekly NFDM price used in the FMMO Class IV formula)

- CME spot call on NFDM (the daily exchange settlement)

- USDA Dairy Market News NFDM series, both high heat and low medium heat splits, across the West, East, and Central regions

- US SMP, the new VPI benchmark, sitting alongside the EU and Oceania SMP VPIs

What this enables for buyers

A US dairy ingredient buyer working an NFDM contract has multiple public reference points to choose from. The Vesper coverage brings them into one workflow and adds a forecast to each.

A global buyer sourcing US-origin SMP for export tenders has a published US benchmark they can write into a contract for the first time, with a forecast attached and the EU and Oceania VPIs sitting beside it for direct comparison.

A trader running US-origin SMP into Europe, North Africa, or Southeast Asia has a continuously updated US SMP price they can read against the EU and Oceania references on a single chart, instead of inferring the US side from NFDM and a guess at the basis.

The specification difference between NFDM and SMP is small in chemistry and large in contract language. Treating the two products as one price flattens the difference at exactly the moment a buyer is trying to manage it. Publishing two distinct prices, each with its own panel and its own forecast, gives the buyer the precision the contract specification already requires.

Want to see the Vesper US SMP price next to the NFDM benchmarks you already track? Vesper publishes the full set of US dairy powder prices, regional and national, alongside the EU and Oceania SMP VPIs, with forecasts and a published accuracy track record on each. Explore the platform.

Frequently asked questions

What is the difference between NFDM and SMP?

NFDM (Nonfat Dry Milk) is the US-standard skim milk powder, governed by US dairy standards and reported through USDA programs and the CME. SMP (Skim Milk Powder) is the international standard, governed by Codex and EU specifications, with a defined minimum protein content of 34% and defined heat treatment classes. The two products overlap heavily in practice and compete in the same global tenders, but they are written into different specifications and do not transact at identical prices.

How is the Vesper Price Index methodology different from a survey-based benchmark?

A VPI is built from confidentially submitted transacted prices from buyers, sellers, and traders, validated against available public references, and published on a fixed schedule with a documented panel. A survey-based benchmark like NDPSR is built from mandatory plant-level reporting under USDA programs. The two are complementary: a VPI is designed to fill categories where a public survey does not exist or does not match the contract specification, while a USDA survey is the regulated reference for the categories it covers.

How accurate are the Vesper SMP forecasts?

The Vesper SMP VPI forecasts hold 96% historical accuracy for EU SMP, 95% for Oceania SMP, and 96% for US SMP at the one-month horizon, measured over the last two years. Accuracy at the three-month, six-month, and twelve-month horizons is published on the platform alongside each forecast and updates as the model accumulates track record.

Can I use the Vesper US SMP price as a contract reference?

Yes. The VPI publishes on a fixed weekly schedule with a documented panel and methodology, which is the structure contract counterparties expect from a referenceable index. Several Vesper customers use VPIs as the indexed reference inside forward contracts already.