WPI, WPC80, MPC70, MPC85, and NFDM have all pushed toward multi-year, and in some cases, historic highs. Tight whey protein supplies have been a major driver, with elevated WPC80 pricing increasingly pulling MPC prices higher as buyers search for alternatives.

The logic behind that shift is understandable. The substitution itself is far less straightforward.

WPC and MPC are both dairy proteins. They serve overlapping end markets and increasingly compete for demand when prices move aggressively. But they are not clean substitutes, either operationally or commercially.

A manufacturer running WPC80 in a beverage system cannot simply replace it with MPC85 overnight without affecting viscosity, solubility, flavor, heat stability, or shelf life. In many applications, reformulation requires technical adjustments, production trials, and in some cases entirely different processing parameters.

That is what makes the current market dynamic so interesting: buyers are still reaching for MPC despite those limitations.

The result is a market where substitution pressure exists, but only partially. Enough to move pricing and procurement behavior, but not enough to create true interchangeability between the two products.

This article explores what MPC is, how it differs from WPC, where both ingredients are used, why substitution is more difficult than it appears, and what current pricing dynamics reveal about dairy protein demand heading into the next twelve months.

What is MPC?

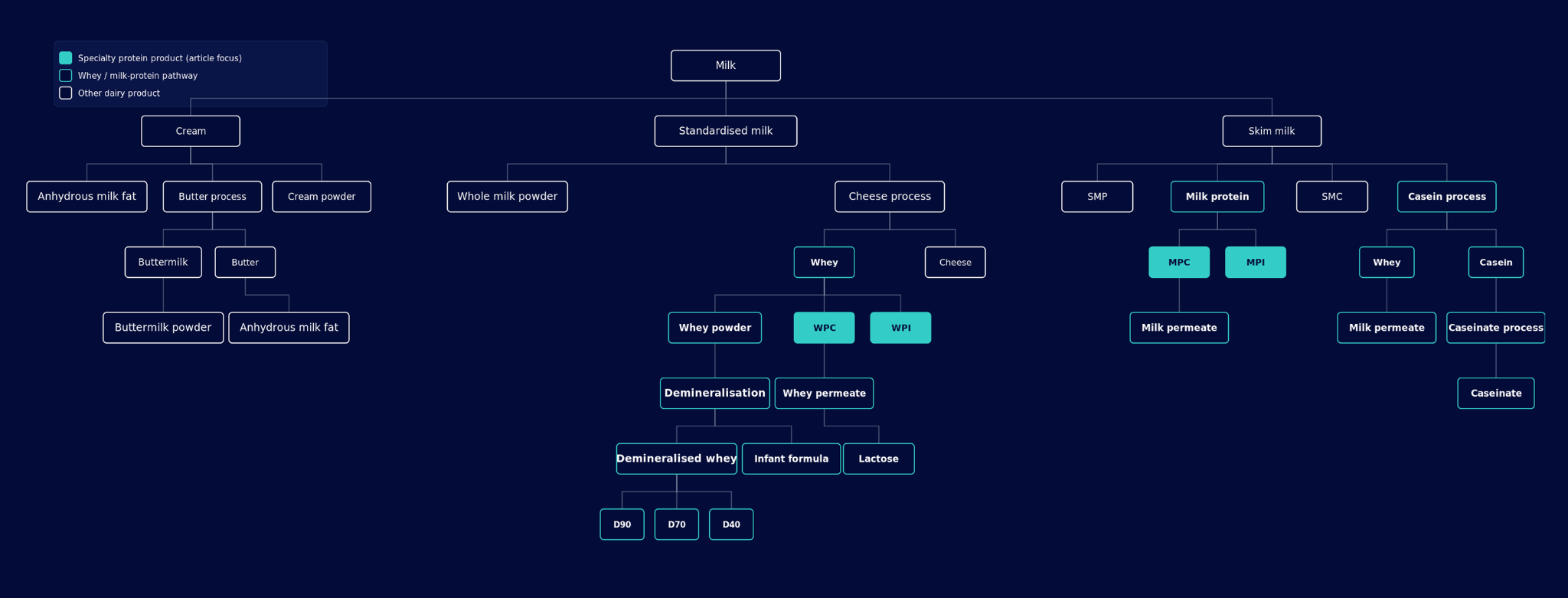

Milk protein concentrate is what you get when you pass skim milk through ultrafiltration to concentrate the protein. The starting material is the same skim stream that produces non-fat dry milk (NFDM) and skim milk concentrate; the difference is how aggressively the membrane filters out lactose and minerals while retaining protein.

The result is a powder that contains both casein and whey protein in roughly the same ratio they exist in native milk, approximately 80% casein and 20% whey. That retained casein-to-whey balance is what distinguishes MPC from whey-protein products like WPC.

MPC comes in a ladder of protein concentrations. The two grades most actively traded in the US are MPC70 (70% protein) and MPC85 (85% protein), with intermediate concentrations also produced. Higher protein content means more aggressive filtration, more processing capacity required, and a higher price per pound.

WPC is built from a different starting stream: cheese whey, the liquid co-product of cheesemaking. WPC contains only whey protein, no casein. WPC34 (34% protein) sits at the low end of the ladder; WPC80 instant (80% protein, with an instantization step so it disperses cleanly in cold water) sits near the top. WPI (whey protein isolate) is the highest end at 90%+ protein, made by running WPC through additional ion-exchange or microfiltration to strip remaining lactose and fat.

Two different starting streams. Two different protein compositions. The same dairy industry, but two different supply chains.

Why isn’t MPC a clean substitute for WPC?

Three reasons MPC and WPC don’t substitute one-for-one.

Functional protein profile. Whey protein is a “fast” protein, it digests quickly and delivers a sharp peak of branched-chain amino acids (BCAAs), which is why WPC80 dominates post-workout sports nutrition. Casein, the bulk of MPC, is a “slow” protein, it forms a soft curd in the stomach and releases amino acids gradually. Both are useful, but they do different jobs. A clinical nutrition formula designed for sustained protein release uses casein-rich MPC by design. A pre-workout shake designed for rapid uptake uses WPC or WPI by design. Swapping one for the other isn’t a tweak, it changes how the product performs in the body.

Sensory and physical properties. WPC80 has a clean profile with a slight whey/dairy note that pairs well with chocolate, vanilla, and other flavor systems used in protein bars and powders. MPC tastes like milk, because it contains intact milk protein, which works beautifully in high-protein milk drinks and yogurts but reads as off-flavor in a flavored sports nutrition shake. Mouthfeel and viscosity differ too: WPC80 dissolves cleanly, while MPC’s casein content gives body and gelation, which is exactly what a high-protein yogurt or processed cheese needs and exactly what a clear protein drink does not.

Solubility in cold water. Sports nutrition powders live or die on cold-water dispersion. WPC80 instant is engineered with a lecithin coating so it disperses in a shaker bottle without clumping. MPC has poorer cold-water solubility because casein doesn’t disperse cleanly without additional functional ingredients or process steps. A formulator who tries to drop MPC into a WPC80 product line without reformulating will produce a powder that clumps in the shaker.

Where partial substitution does work is in protein-enriched products that already accept some formulation latitude, high-protein milk drinks, fortified yogurts, protein-fortified bakery and cereal products. In those applications, blending up to 10–20% MPC into a system that previously ran on WPC80 is increasingly considered viable. It’s the distinction between full substitution, which doesn’t hold up in clean-label sports nutrition powders, and partial blending, which works in a meaningful slice of the protein-enriched category.

So when a buyer in clean-label sports nutrition says “we’ll use MPC instead because WPC is short,” they’re committing to a reformulation project, not a procurement swap. In protein-enriched applications with more formulation flexibility, the swap is already happening.

When would a producer choose WPC over MPC?

WPC80 is the workhorse in any application where the protein needs to perform fast and the powder needs to disperse in cold water without help. That covers sports nutrition shakes, post-workout drinks, ready-to-mix powders, protein bars where high BCAA content is part of the marketing claim, and clear protein beverages where WPI specifically is preferred for its cleaner flavor.

WPC also wins where formulators are pricing per gram of protein and the cleaner whey-protein profile is what consumers expect. Most direct-to-consumer protein supplements live in this category.

When would a producer choose MPC over WPC?

MPC wins anywhere a complete dairy protein matters, where mouthfeel and structure are part of the eating experience, or where slow protein release is part of the nutritional design.

That includes high-protein milk drinks (the casein contributes the body that makes a 30g protein milk taste like milk and not like water), high-protein yogurts (casein is part of the structure), processed cheese, clinical and medical nutrition formulas (sustained release plus complete amino acid profile), and infant formula (the casein-to-whey ratio is part of the spec).

Most of these categories have grown sharply over the last two years. The consumer-level signal sits in the retail data: Chobani’s high-protein Fit range jumped 50% year-on-year, Bega Group expanded into high-protein full cream milk in a category that has grown 48% over five years, and Woolworths’ CEO described demand for high-protein yogurts as “incredible.” None of these are WPC categories, they are MPC categories by formulation.

So why are buyers reaching for MPC right now?

Two reasons, and they cut in different directions.

The first is real demand growth in MPC’s native categories. McKinsey’s 2026 Dairy Executive Survey put it in numbers: 88% of US dairy executives called protein the most influential consumer trend, far ahead of convenience or premiumization. That trend is showing up most in the high-protein consumer dairy SKUs that use MPC for structural reasons. GLP-1 adds another layer: Circana found nearly a quarter of US households now have at least one active GLP-1 medication user, and the consumer behaviour shift inside those households favours protein-forward food. So MPC is being pulled by genuine demand growth in its own categories, not just by spillover.

The second is spillover from a short WPC market. WPC supplies have been described in Vesper’s own market commentary as “remarkably short,” and that scarcity has started to pull MPC prices up. The math behind the swap is simple: at current price levels, every kilogram of WPC80 a formulator can replace with MPC85 saves roughly €15. That gap is large enough that procurement and product development teams are working through reformulation cases side by side, rather than waiting on whey supply to recover. MPC is not the only ingredient catching that bid, SMP, ultrafiltered milk, caseinates, and even plant-based proteins are all in the conversation wherever the formulation tolerates them, but MPC sits closest in profile to WPC and tends to get first look.

That shift was on full display at the ADPI conference earlier this month. Participants were actively chasing spot WPC volumes with little regard for price, and the hallway conversations around reformulation were running just as hot as the bidding on the floor. Buyers are simultaneously securing supply at historically high levels and quietly evaluating how much of next quarter’s spec can move to MPC, blends, or other dairy proteins without breaking the product. MPC85 prices in both Europe and the US are already moving up quickly as a result, and Q3 demand is building on top of an already tight market.

Both forces are real. Both are pulling MPC demand higher at the same time.

What’s happening to US MPC supply?

While demand was building, US MPC production was contracting.

The cleanest data point: US MPC production dropped 11.8% in early 2026, down to 26 million pounds. The pattern behind it, US processors have been quietly but clearly rotating away from commodity milk powders and toward higher-value whey proteins. NFDM and MPC are losing ground to WPC80 within the skim solids mix.

By mid-March, the framing was sharper. NFDM, MPCs, and WPCs were named as the categories in real supply shortage, even as export headwinds weighed on the rest of the US dairy complex. The protein-bullish read held.

A real supply shortage, called out by name.

A structural amplifier landed at the same time. The US-India trade deal, finalised in late January 2026, liberalised tariffs on milk protein concentrates, with full liberalisation phased in over seven years from the previous 20% duty. A new export demand channel opened at the same moment domestic production was shrinking.

Capacity expansion is on the planning horizon for several producers, and headline MPC output is up modestly in some regions, but neither is sized to absorb the additional whey-spillover demand layered on top of MPC’s own native growth. The market the industry built for 2026 is smaller than the demand the industry is now trying to push through it.

Demand up. Supply down. Export channel widening. Three forces walking in the same direction at the same time. That is the MPC story heading into mid-2026.

How do you put a price on MPC?

Two paths a buyer can take.

Path 1 the calculation route. Anchor on NFDM and apply a multiplier. Vesper has walked through this exercise for MPC85 directly: average multiplier of 3.288× NFDM, with a working range from 2.73× in early February 2026 to 3.68× in mid-October 2025. Vesper’s own framing of the proxy: the NFDM multiplier is a useful monitoring tool for skim-side MPC85 movements, not a settlement-grade calculator. WPC and MPC serve distinct applications, and their prices can diverge fast, the whey-MPC connection has broken loose.

Adding to the noise, the proxy itself has been moving. With NFDM rising sharply in recent weeks, applying a 3× multiplier amplifies every move on the skim side directly into the MPC85 print, even when MPC’s own fundamentals are pointing in a slightly different direction. That is the right read for what the proxy is, a monitoring tool. It is not a settlement-grade calculator. At a 2.73× to 3.68× range, a buyer pricing a forward against the long-run average can be off by a meaningful margin on a real contract.

Path 2 the direct route. Vesper publishes weekly VPI benchmarks for US MPC70, MPC85, and MPI90 anchored on transacted prices from the panel. No multiplier required. The VPI is built specifically to fill the gap left by the lack of official US reporting on specialty proteins like MPC70, MPC85, and WPC80, products that don’t have an equivalent USDA benchmark or a CME contract.

Use the proxy when reading direction. Use the direct VPI when writing the contract.

Where do US MPC prices go from here?

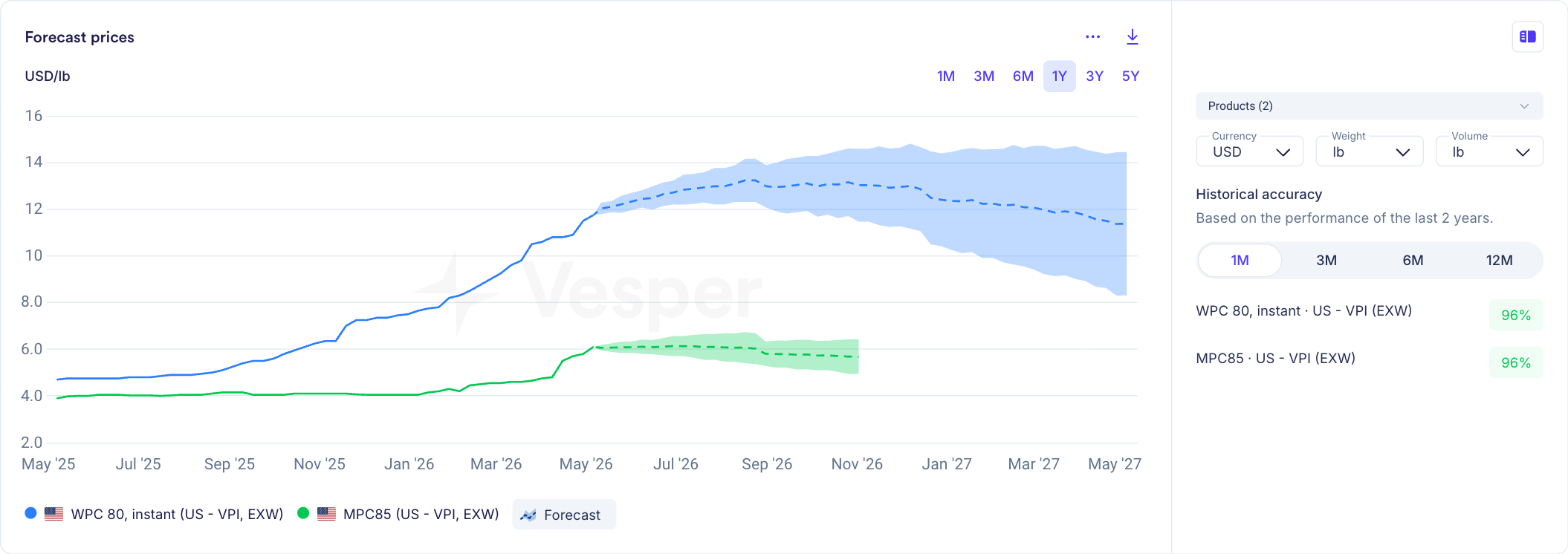

The benchmark answers “what’s the price today.” The next question for procurement is “where does it go.” Vesper publishes a forward forecast layer alongside every VPI series, with confidence bands and rolling historical-accuracy figures so a buyer knows how much weight to give a particular horizon.

For US MPC85, historical accuracy currently runs at 96% on a 1-month forward, 90% at 3 months, and 88% at 6 months. The forecast extends six months out with a confidence band that widens with horizon.

Vesper VPI forecast, US WPC80 instant and US MPC85, May 2026 snapshot.

For US WPC80 instant, the same horizons read 96%, 88%, and 80%. MPC85 holds up slightly better at the longer end, milk-protein moves track upstream NFDM cycles more cleanly than whey-side moves track dry whey.

The current six-month read on MPC85 shows the price flattening from the May 2026 highs and easing through Q3 inside a tightening confidence band. WPC80 instant follows a similar trajectory at higher absolute levels, though the structural deficit in whey is not expected to reverse in the short term, and the reformulation pull on MPC looks durable rather than transient.

Vesper’s forecasts come from a foundation-model architecture trained on transacted prices, supply-and-demand fundamentals (production, stocks, exports), futures markets, and cross-commodity moves. Each VPI series gets its own forward curve plus rolling historical-accuracy figures so a buyer can decide how much to lean on the forecast for a specific contract horizon. The model retrains continuously and is benchmarked against actual realised prices.

The shift this creates for procurement teams: budget conversations move from “what’s our anchor for the year” to “what’s the most likely curve through the year and how wide is the range around it.”