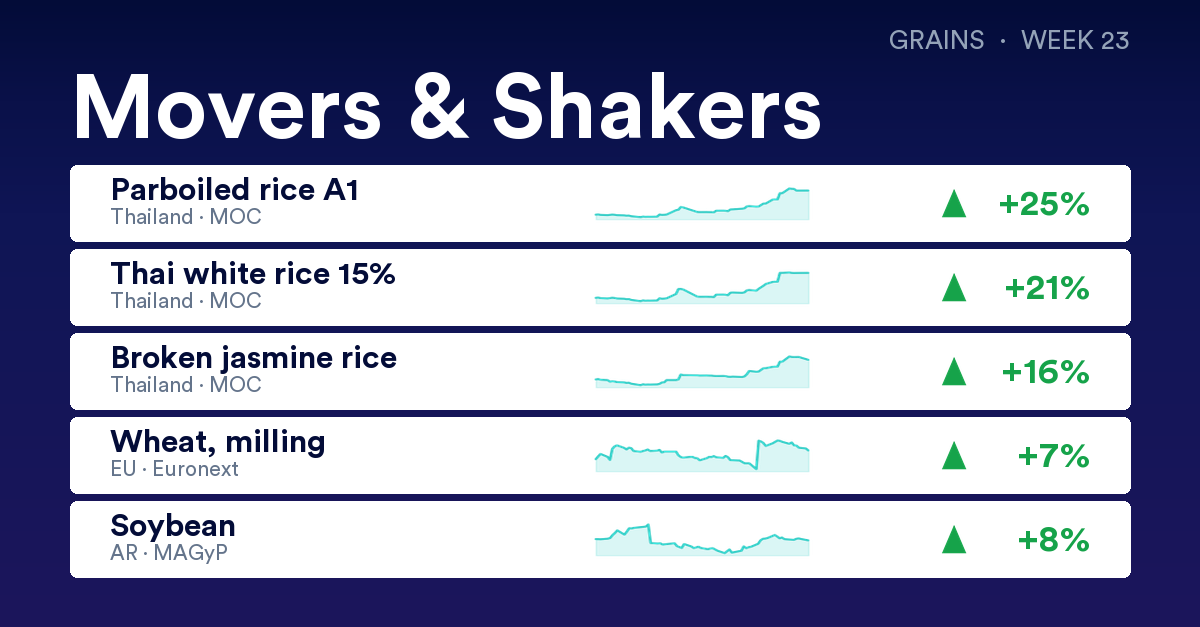

Thai rice prices rose between 16 and 25 percent in May, with parboiled rice A1 leading the move from 220.73 to 275.61 USD/mt. But the month was not only a rice story. EU milling wheat fell to 180 EUR/mt on 11 May then jumped 36 EUR/mt the following session, and Argentine soybean reversed a multi-week decline to close the month 8 percent above where it started. Across grains, May was a month of sharp repositioning.

The movers

The Thai rice move had been building for almost a year. According to Vesper’s Biweekly Rice Market Report (Week 17), flooding across Punjab, Haryana, Uttar Pradesh, Bihar, and Rajasthan destroyed 40 to 42 percent of India’s basmati paddy output last July. By April 2026, mills that normally ran on 20-day credit terms were demanding advance payment before releasing anything, with fresh arrivals running at 20 percent of normal.

Through April and into early May, Thai MOC benchmarks drifted into a soft correction as export margins compressed. Bunker fuel costs rose roughly 50 percent following renewed tensions in the Iran corridor, and a Chinese import suspension on GMO grounds added to cautious sentiment. Thai white rice 15% broken slipped to around 288 USD/mt by 5 May. Buyers who expected more downside held off.

On 21 May, that waiting ended. Vesper’s Week 23 report notes that exporters covering May and June shipments went to mills and found almost nothing available at workable prices. Parboiled rice A1 gained the most at nearly 25 percent, reaching 275.61 USD/mt. Thai white rice 15% broken crossed 349 USD/mt, and broken jasmine rice reached 346.82 USD/mt, both up more than 15 percent from where they started the month. The USDA projects the 2026-27 global rice balance falling 5 million tonnes short of consumption, with no meaningful new supply before October.

Wheat told a different story. EU EuroNext milling wheat fell to a monthly low of 180 EUR/mt on 11 May, driven by the US-China trade summit’s failure to produce concrete soybean purchasing commitments, which triggered fund liquidations across the grains complex. According to Vesper’s Bi-Weekly Grains Week 21 report, even a rising Brent crude price, up to $112 as fresh Middle East attacks escalated, could not stop the sell-off. The following session, wheat jumped to 216 EUR/mt as record May temperatures in France, the UK, and Spain raised supply concerns at a sensitive spring growth stage. US winter wheat conditions were running well below average, with just 28 percent rated good-to-excellent against 52 percent a year earlier, per the same report. By 2 June, EuroNext had settled at 204 EUR/mt, still 6.5 percent above where it started May, but with significantly more volatility than the month-on-month number suggests. Vesper’s Week 22 grains outlook flags Brent as a key ongoing price risk: if a US-Iran ceasefire materialises and the Strait of Hormuz reopens, easing energy premiums could weigh on European grain prices through Q2.

Argentine soybean closed the month at 279.93 USD/mt, up 8 percent from 259.10 USD/mt on 1 May. The mid-month slide toward 258 USD/mt was triggered by the same US-China summit disappointment: the talks produced no specifics on additional soybean purchasing commitments, driving fund liquidations across the soy complex, per Vesper’s Bi-Weekly Grains Week 21 report. Weaker Brent in the second half of May added to the pressure before prices recovered as Iran suspended ceasefire talks and Brent rebounded.

Worth watching

The Thai rice floor looks more durable than the April correction suggested. The moves after 21 May held as physical buyers absorbed the new price level rather than fading. With Gulf and GCC restocking expected to build through June, the supply window that existed in April has closed.

Keep tracking grains prices in real time on Vesper.