Vesper has modelled three commodity price scenarios based on the Brent price. The duration of the Middle East conflict and impact on oil infrastructure is important for Brent.

Best case – Brent at $80/barrel

Conflict ending in 1–2 weeks, with limited infrastructure damage. Vegetable oil, grain, and sugar prices return close to pre-conflict levels. Freight rates begin declining as passage through the Strait of Hormuz resumes. Urea eases from its current ~$650/mt spike but likely retains a risk premium for up to six months.

Medium case – Brent at $100–120/barrel

A weeks-long Strait closure with moderate infrastructure damage. BMD crude palm oil rises to $1,250/mt, Euronext wheat to $360/mt, and Sugar no. 11 (US – ICE) to 22 US cents/lb. Urea spikes to $900/mt before settling around $500/mt. Freight rates remain broadly sideways.

Worst case – Brent at $135–150/barrel

A prolonged closure with severe infrastructure damage and force majeure declarations. Prices reach multi-year highs across all commodities, palm oil at $1,550/mt, Euronext wheat at $430/mt, Sugar no. 11 (US – ICE) to 25 US cents/lb., and urea above $1,000/mt. The fertilizer shock would be severe, given the region’s share of global urea (44%), ammonia (27%), and phosphate (25–36%) exports. Macro conditions turn stagflationary.

Best case scenario – Brent at $80/barrel

Scenario assumptions

- Conflict duration and closure of the Strait of Hormuz from now on expected to last 1–2 weeks, with de-escalation starting shortly.

- Oil infrastructure damage and capacity suspension expected to remain limited, with the quickest repairs taking from a few weeks to a couple of months.

- Additional factors that could bring Brent prices down include navy convoys restoring shipping through the Strait of Hormuz, the provision of low-cost political risk insurance by the US for ship owners, and the release of national reserves.

Vesper scenario modelling, based on a Brent price of $80, suggests that vegetable oil prices could return close to the levels seen before the start of the conflict. Prices for key oils before the beginning of the conflict:

- BMD crude palm oil price $1,026/mt. A fall to $1,000/mt or below is possible due to high Malaysian stocks

- CBOT crude soybean oil 60–61 US cents/lb. If the US finalizes biofuel policies in March and establishes high mandates with favorable rules, prices will be supported

- 6 ports crude sunflower oil $1,350–1,400/mt. The arrival of sunflower seeds from Argentina to Europe could weigh on prices

- FOB Dutch Mill crude rapeseed oil $1,200–1,250/mt

- EXW Manila crude coconut oil $2,100/mt

- DAP Malaysia crude palm kernel oil $1,800–1,850/mt

Grains

- Wheat Euronext: $225–230/mt

- Corn Euronext: $225/mt

- Soybean CBOT: 1160 USD cents/bu

Sugar

- No. 11 US – ICE: 13.9–14 USD cents/lb

Freight

Freight may start declining as soon as the traffic through the strait of Hormuz starts increasing. News about convoys and insurance can help as well. Freight will decrease largely within 1–2 months after the end of the conflict, with potential return to the pre-crisis levels in the longer term.

Fertilizer impacts

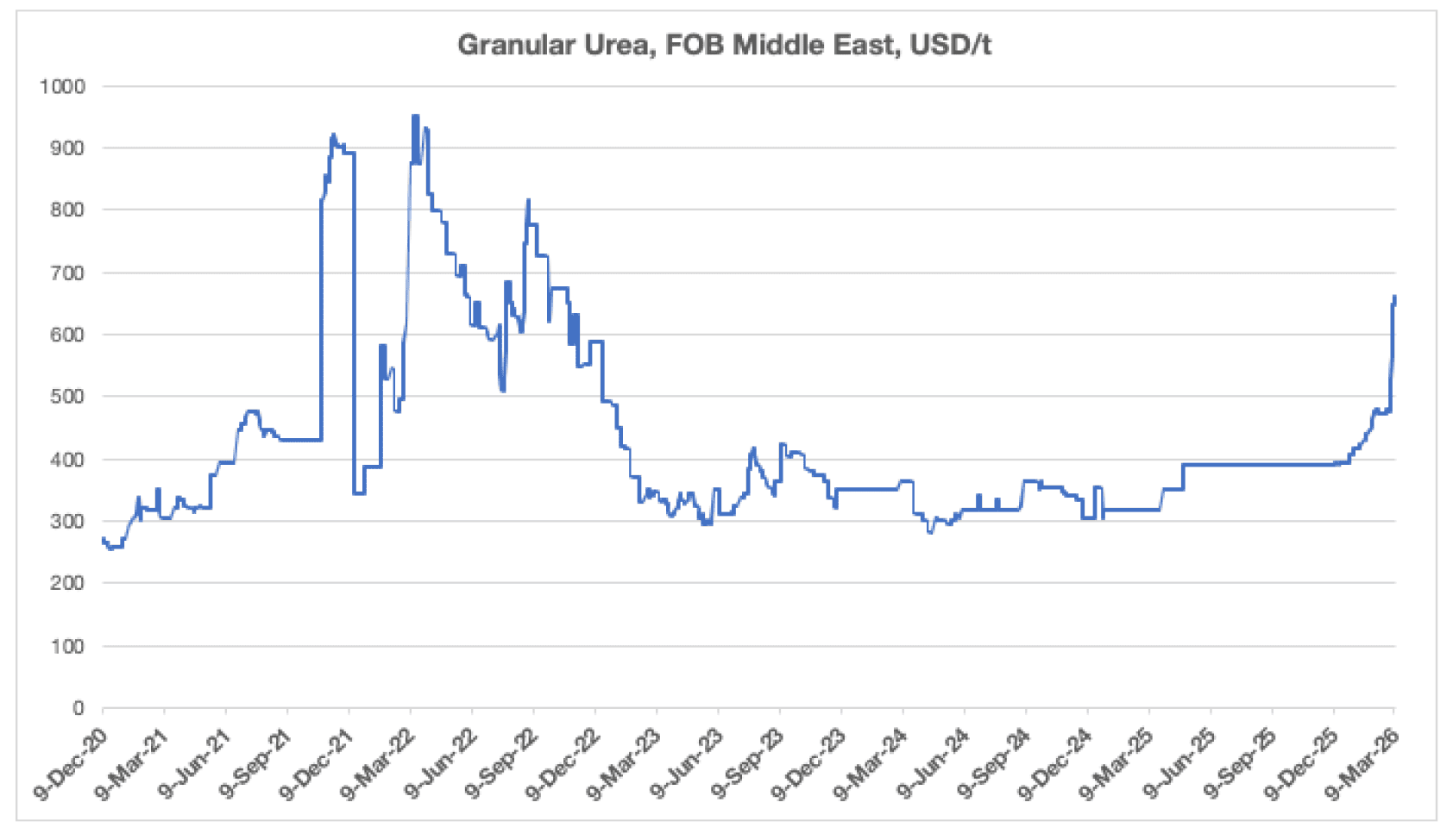

- Urea granular, FOB Middle East = stable around 500 USD/t (from 484 USD/t pre conflict).

In this scenario we see lower risk of extended disruption to fertiliser flows, meaning recent price spikes of 650 USD/t could fall back, a rapid de-escalation would see prices dip but likely retain some risk-premium for the next 6 months as markets could remain quite jittery. In response to effects of the June 2025 conflict urea prices kept their premium for the following 6 months.

Broader risk market macro impacts

- EUR/USD – 1.155 = due to lingering safe-haven effects. Potential recovery back to 1.165.

- Gold price = has retreated but from an already high valuation, see around current levels of 5,200 USD/oz. No comparable ref case due to specifics of current gold price valuation – never had a conflict break out with gold already trading at record highs.

First rate cut by US Fed – July 2026, 25 bps. Equities – US outperforms EM, Europe. Energy, materials, healthcare outperform other sectors. After geopolitical shock markets mostly return to positive territory, estimated by Man Group as 62% of the time, with an average positive return one month after the event of 2%.

As of Monday 9th March markets have begun to price a more extended conflict with longer closures to shipping of oil, oil products and gas. This means that in the best scenario case, with limited disruption, we could see a rebound in risk assets. Markets were already grappling with the impact of AI on earnings, and with stresses in private credit markets, meaning that recent downside was somewhat exaggerated, most often markets respond to geopolitical risk with a sell the rumour, buy the fact response, whereupon the uncertainty before conflict erupts is worse for asset pricing. Economic impact from a short spike in energy costs would be less for importing regions, and we would not see a need to revise growth or inflation in this scenario.

Medium case scenario – Brent at $100–120/barrel

Scenario assumptions

- Weeks-long closure of the Strait of Hormuz, with a partial release of strategic petroleum reserves.

- Oil infrastructure damage and capacity suspension expected to be limited to moderate.

- Natasha Kaneva, head of global commodities research at JPMorgan Chase, warned that Gulf countries’ oil storage capacity could be exhausted within three weeks, potentially forcing production to halt. In this scenario, oil prices could surge to $120/barrel. Axios and Rapidan Energy Group have echoed the possibility of $120 oil.

Vesper scenario modelling for vegetable oils if Brent reaches $120:

- BMD crude palm oil $1,250/mt

- CBOT crude soybean oil 77 US cents/lb

- 6 ports crude sunflower oil $1,650/mt

- FOB Dutch Mill crude rapeseed oil $1,500/mt

- EXW Manila crude coconut oil $2,450/mt

- DAP Malaysia crude palm kernel oil $2,150/mt

Grains

- Wheat Euronext: $360/mt

- Corn Euronext: $330/mt

- CBOT soybean: 1590 USD cents/bu

Sugar

- No. 11 US – ICE: 22 USD cents/lb

Freight

As per market sources, freight rates have limited room to move higher and are more likely to remain sideways or see a modest correction. Demand may struggle to sustain current rate levels, while vessel supply remains tight due to ongoing rerouting. Some shipowners are avoiding the Suez Canal, which is extending voyage times between Asia and Europe.

Fertilizer impacts

- Urea granular, FOB Middle East = spike to 900 USD/t, settle around 500 USD/t.

With this scenario involving a suspension of shipping traffic and possible infrastructure damage that could impact production infrastructure we would see a spike of prices close to 2022 levels, once traffic resumes there would be quick de-escalation but considering infrastructure restart unknowns, prices could stay relatively higher for longer.

Broader risk market macro impacts

Some pass through from higher crude and disruptions, but likely short-term:

- EUR/USD = 1.1125

- Gold price = 5200 USD/oz

First rate cut by US Fed = Q4 2026.

Worst case scenario – Brent at $135–150/barrel

Scenario assumptions

- Weeks/months closure of the Strait of Hormuz.

- Severe oil infrastructure damage and/or production suspensions, with declarations of force majeure. Recovery could take months to years. In one of the worst-case scenarios, Iran’s key export terminal at Kharg Island could be destroyed.

- Saad al-Kaabi, Qatar’s energy minister, warned that regional producers could soon be forced to halt production, and that prices could reach $150 per barrel, adding that companies that have not yet declared force majeure are expected to do so in the coming days.

- ExxonMobil and Kpler estimate that oil could reach around $135 per barrel in a severe disruption scenario.

Vesper scenario modelling for vegetable oils if Brent reaches $150:

- BMD crude palm oil $1,550/mt

- CBOT crude soybean oil 95 US cents/lb

- 6 ports crude sunflower oil $1,900/mt

- FOB Dutch Mill crude rapeseed oil $1,750/mt

- EXW Manila crude coconut oil $2,800/mt

- DAP Malaysia crude palm kernel oil $2,500/mt

Grains

- Wheat Euronext: $430/mt

- Corn Euronext: $390/mt

- CBOT soybean: 1850 USD cents/bu

Sugar

- No. 11 US – ICE: 25 USD cents/lb

Freight

Freight rates will stay firm in the short term, but within several month time can decline due to the demand rationing and slower global business activity.

Fertilizer impacts

Very high prices are expected in this scenario, the shock could be worse than the impact of the 12-day Israel-Iran war in 2025, and also worse than 2022. In 2022 Russian exports continued, in this scenario there would be no export flows, impacting 44% global urea exports, 27% global ammonia exports, 25% global phosphate fertilizer exports, 36% global phosphate rock exports, 47% of global sulphur exports and 9% of global potash exports.

Removing these volumes from the market would have a price impact on fertilizers themselves and also a lingering impact on crop yields further out. Urea granular, FOB Middle East = 1000 USD/t (from 484 USD/t pre conflict), already trading 700 USD in spot. Keeping forecast just above highs of 2022, with potential to spike above this level. US and Latam would be more insulated from food supply effects.

For Europe, risk channel is via Egypt and Algeria who supply over 30% of imported nitrogen and ammonia, and via the spike in TTF which impacts the cost of European nitrogen manufacturing.

Broader risk market macro impacts

Stagflationary environment created by weaker growth and higher inflation:

- EUR/USD – below 1.0 (ref. 2022 Energy crisis)

- Gold price = 5500 USD/t, entering conflict at record highs

First rate cut by US Fed – unclear for 2026, broader downturn could necessitate action to be brought forward although inflationary effects should suggest no cut for 2026. If inflation extends and labour demand weakens, a US recession could become a possibility. This brings global markets further under pressure, giving more upside to gold and USD as safehavens. Asia sees the highest energy related cost pass through, impacting growth which was already weakening in China (Official GDP target recently revised to 4.5–5% for 2026). EM outflows have by 9th March exceeded those of 2020 and 2022, EM markets had gained a lot going into this, meaning there was room for reversal. Further drawdowns in major Asia equity indices, and broad currency weakness vs USD to be expected. Asia policymakers have tools to cushion the blow with market stabilization measures and caps to domestic fuel prices, and will deploy these should the worst case scenario unfold. EU HICP – avg for 2026 rises to 3%, ECB rate hike seen possible in summer 2026.