While flavour remains a key consideration, the choice between butter and vegetable oils in industrial baking reflects evolving consumer expectations, and has broader implications for brand perception, health positioning, supply chain resilience, and the bottom line.

Major players like Kraft Heinz, Hostess Brands, and Grupo Bimbo have all reengineered iconic products to meet these shifting demands. Think Triscuits and Wheat Thins with cleaner labels, Twinkies with longer shelf lives and no trans fats, or Marinela Mini Mantecadas tailored to local markets without sacrificing cost control.

To make the right call, procurement teams must go beyond cost and evaluate fat choices through a strategic lens. In 2026, five key factors should need some consideration when making these decisions:

1. Cost pressures

In 2025, cost remains the unshakable constant in fat selection, but it has become a more strategic balancing act, shaped by commodity volatility, margin pressures, and global trade dynamics.

Major FMCG players are feeling the squeeze. Nestlé India posted a 12% drop in net profit for Q1 2025, despite a 6% rise in revenue, largely due to rising input costs. Procter & Gamble announced price hikes on about 25% of its U.S. products to offset new tariffs.

Against this backdrop, understanding the cost behavior of key baking fats is critical. Butter and palm oil, two of the most widely used fats in industrial baking, offer a focused lens on the trade-offs procurement teams must navigate. While other oils like canola, sunflower, coconut, and olive play important roles, this comparison captures the core dynamics influencing fat strategy.

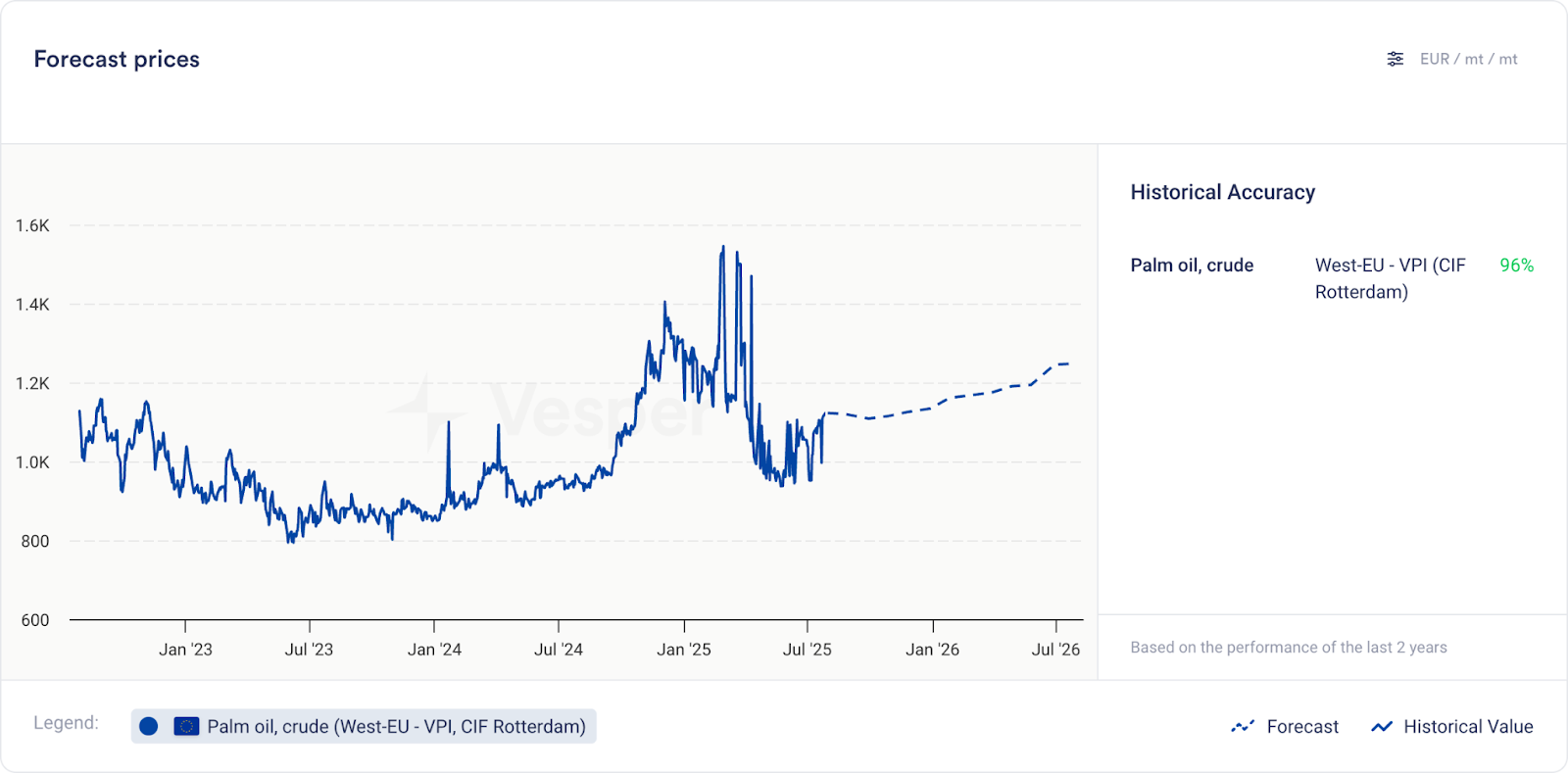

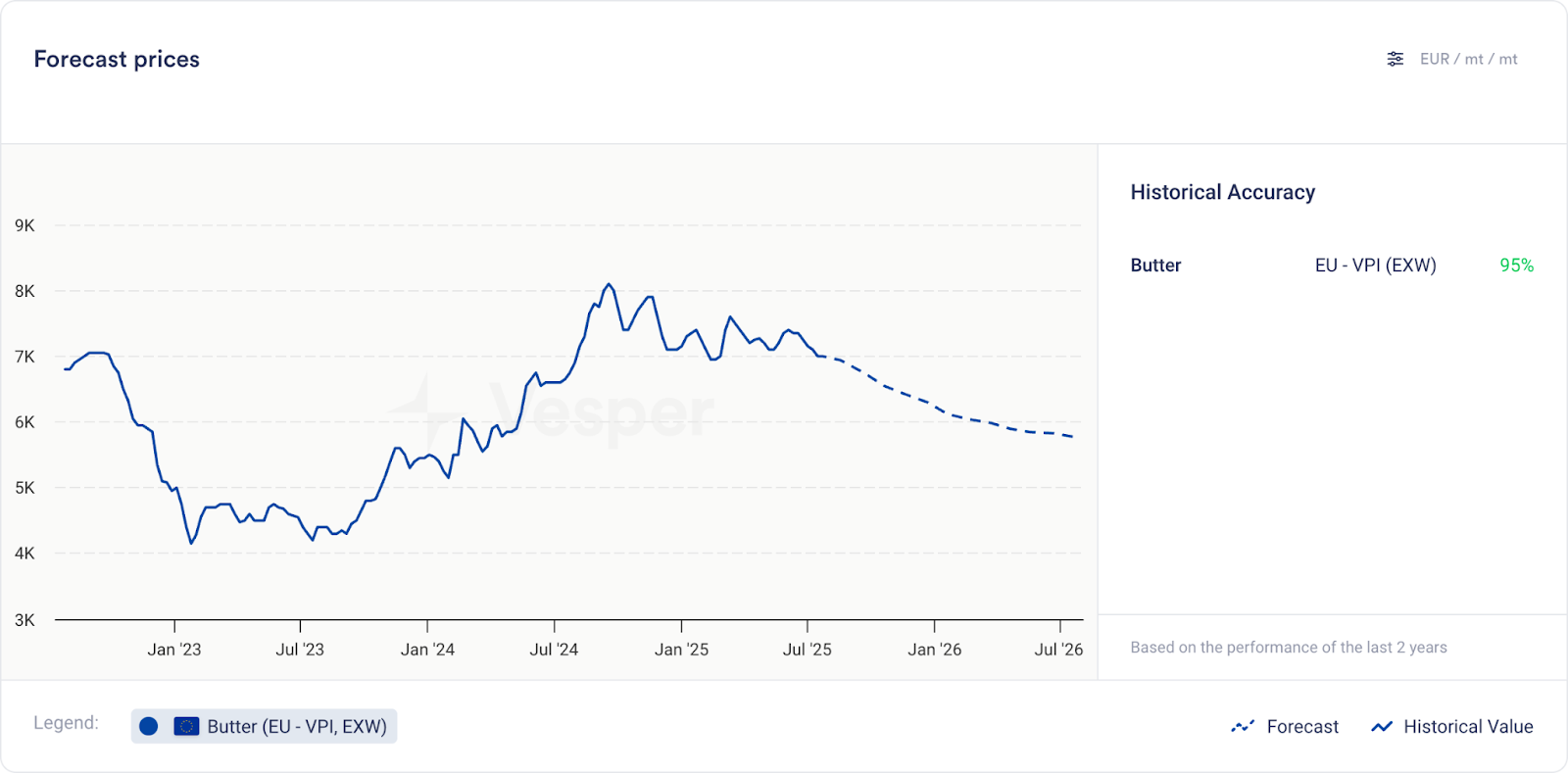

To illustrate, Vesper’s AI-driven price forecasts for butter and palm oil provide a real-time example of how data can support smarter, forward-looking sourcing decisions, especially when cost predictability and margin protection are on the line.

Butter remains far more expensive than palm oil, despite forecasts for a gradual price decline. As of July 2025, European butter prices are under pressure due to higher milk output and sluggish exports, but they remain well above vegetable oil benchmarks. Palm oil, on the other hand, has dipped slightly following strong Malaysian production and weaker exports, though Vesper expects a recovery in late 2025, fueled by rising demand from India and China and tightening Indonesian supply.

Procurement leaders should be aware that while palm oil dominates cost-effective formulations, other oils bring unique pricing and risk profiles, especially in health-focused or region-specific SKUs.

2. Supply stability

A competitive price offers little value if the ingredient can’t be sourced consistently, at scale, and in compliance with tightening regulations. In 2026, both butter and vegetable oils face very different, but equally important, supply-side risks that procurement teams must factor into their planning.

Butter: Tightening supply at the farm level

On the dairy side, availability is increasingly tied to structural constraints in milk production. While some European regions have seen higher milk output in mid-2025, this may not last. Herd sizes in key producing countries are gradually declining due to environmental pressure, cost of feed, and low farmgate margins. In places like Germany and the Netherlands, farmer exit rates have increased, particularly among small-to-mid-sized operations. Any tightening at the raw milk level ultimately cascades into cream and butter production, creating a fragile upstream.

Moreover, the growing regulatory burden across Europe is compounding the issue. Stricter environmental policies, including nitrogen caps and land-use restrictions, are reducing long-term expansion potential for dairy herds. While butter availability has held steady so far, there’s little cushion in the system. A harsh winter or drought in 2026 could quickly create volatility, especially coupled with rising export demand.

Vegetable Oils: geopolitics, climate, and regulation

Vegetable oils, though more diversified in origin, face their own unique risks, many of which are becoming more acute. Weather remains the most immediate concern. In 2025, harvesting delays for rapeseed across the EU due to unseasonal rainfall, combined with reduced Ukrainian yields and heat stress in Canada and Australia, have already strained availability. Sunflower and soybean crops have also shown vulnerability, with weather-related setbacks repeatedly disrupting supply expectations.

Then there’s the growing impact of regulation. The EU Deforestation Regulation (EUDR), set to apply from 2025 into 2026, poses a significant compliance burden for palm, soy, and cocoa, and by extension, the baked goods that use them. While many multinational suppliers are investing in traceability, some processors are struggling to meet due diligence thresholds. This may reduce the volume of compliant oil available to the EU market, creating fragmentation in global supply chains and tightening access, especially for palm oil.

Coconut oil, used in many clean-label or plant-based SKUs, also faces availability risk due to cyclical production swings and aging tree populations in the Philippines and Indonesia.

3. Shelf life

With food waste costing the baking industry billions annually, the shelf life is an important factors to take into consideration. As highlighted by Kerry, “Mould causes 65% of global bakery waste”, making fat selection a crucial lever in minimizing losses.

Butter and vegetable oils affect shelf stability in fundamentally different ways. While butter delivers richness and brand appeal, it introduces more water, dairy proteins, and oxidation risk, all of which can shorten microbial and flavor shelf life. Vegetable oils, particularly refined and high-oleic variants, offer a longer-lasting alternative, especially in products where neutral flavor and soft texture are key.

Here’s how the two compare across critical shelf life dimensions:

Butter vs. Vegetable Oils: Impact on Shelf Life

| Feature | Butter | Vegetable Oils (e.g. canola, sunflower, palm) |

| Oxidative Stability | Lower – contains saturated & short-chain fatty acids prone to rancidity | Higher (for refined oils) – especially if high in monounsaturated fats (e.g. canola, high-oleic sunflower) |

| Water Content | ~15–18% water (butter is ~80% fat) → increases water activity, reducing shelf life | Nearly 100% fat, with no water → lowers water activity, extends shelf life |

| Flavor Stability | Prone to off-flavors over time due to oxidation & Maillard byproducts | More neutral; less risk of flavor degradation (except for some unrefined oils) |

| Microbial Shelf Life | Shorter – water + dairy proteins promote microbial growth | Longer – no proteins or water = less microbial risk |

| Staling Rate | Butter-based goods often stale slightly slower due to solid fat matrix | Oils may not delay staling as effectively (depends on structure & formulation) |

| Storage Requirements | Needs refrigeration in some formats | Shelf-stable under most conditions |

Even if butter is chosen for its premium positioning or sensory quality, there are effective ways to mitigate its shelf life limitations. Two key strategies are redefining your formula with shelf life-enhancing ingredients (like enzymes, natural preservatives, or antioxidants) and investing in protective packaging such as MAP or barrier films. On Vesper, you can access pricing data for both ingredients and packaging materials, now strengthened by our partnership with Fastmarkets, giving you the transparency to make informed, shelf-life-optimized decisions.

4. The clean label trend

Consumer expectations around baking fats are shifting rapidly, driven by growing attention to health, sustainability, and ingredient transparency. Oils like canola, soybean, and olive are gaining favor thanks to mounting clinical research linking plant-based fats to reduced mortality and improved cardiovascular health. At the same time, butter, while still valued for flavor and simplicity, is increasingly scrutinized for its saturated fat content and environmental impact.

To translate these health trends into consumer trust, procurement teams should also factor in clean label compatibility. An increasing number of bakery companies are reformulating products to meet clean‑label standards, responding to significant consumer demand for simplicity, transparency, and trust in product ingredients. In fact, nearly 30% of all new food and beverage launches now carry a clean‑label claim, and 79% of R&D teams report clean label as a top innovation priority, according to Innova Market Insights.

While it’s not legally defined, it consistently includes a few core pillars that guide how consumers and brands interpret it, like health-related factors, environmental impact, and Transparency & Traceability. Here’s a structured breakdown of the most widely recognized dimensions of clean label relevant to using butter vs. vegetable oil in baking products:

Clean label impact: Butter vs. vegetable oils in baking

| Clean Label Dimension | Butter | Vegetable Oils (e.g. canola, sunflower, soybean) |

| Ingredient Simplicity | Single-ingredient, recognizable (“butter”) | Recognizable when labeled clearly (“canola oil”); refined blends may raise concerns |

| Allergen & Diet Suitability | Contains dairy; excludes vegan and lactose-free claims | Suitable for vegan, dairy-free, and often allergen-free products |

| Processing Level | Minimal – traditional churning | Varies – cold-pressed oils are clean; refined oils involve more steps |

| Need for Additives | May need mold inhibitors or shelf-life extenders in ambient bakery formats | Often needs emulsifiers or enzymes to mimic butter structure |

| Environmental Footprint | Higher GHG emissions, land and water use (animal agriculture) | Generally lower – but varies: e.g. palm oil raises sustainability concerns |

5. Reformulation demands

Swapping one fat source for another is rarely a plug-and-play solution. In industrial baking, even a small change in fat type can trigger a cascade of formulation adjustments to preserve taste and texture and maintain product structure, shelf life, and labeling compliance.

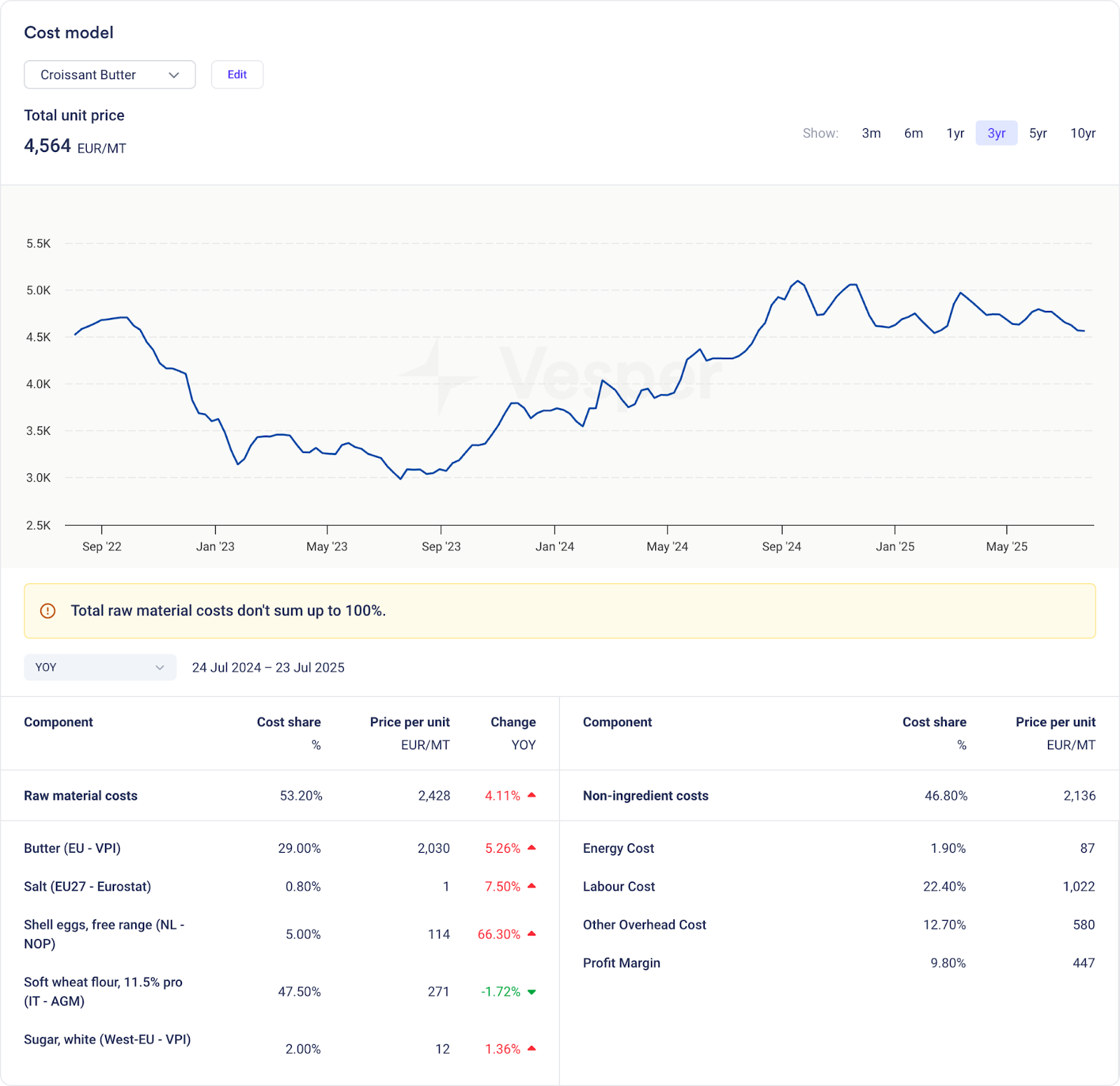

Consider the croissant. Replacing butter with a vegetable-based alternative like palm or sunflower oil might lower fat costs significantly, but the impact goes far beyond price per kilo. Butter isn’t just a flavor contributor; it plays a critical role in lamination, steam generation, and texture. When it’s removed, the dough’s behavior changes. To compensate, manufacturers often need to adjust water content, flour strength, and emulsifiers. Even the type of yeast or resting time may require optimization to recover the original flake and rise.

Vesper’s cost model comparisons, one for a butter-based croissant and one using margarine, clearly demonstrate how dramatically the ingredient mix and input costs shift with a change in fat type. These models not only highlight the savings potential but also expose the downstream formulation and sourcing implications.

While replacing butter leads to clear savings on fat costs, it also alters the sourcing strategy for other ingredients and impacts the production process. Everything from ingredient origin and label claims to the settings on lamination equipment may need to be reviewed and adjusted. The final product may meet margin targets, but not without careful recalibration across the full ingredient deck.

All in all,

In 2026, procurement decisions between butter and vegetable oils should consider five key factors: cost pressures, supply stability, shelf life performance, clean label compatibility, and reformulation complexity. Each fat type brings unique trade-offs, and selecting the right one requires balancing functionality, consumer expectations, and long-term supply chain resilience.