What Are Sugar Futures?

Sugar futures are standardized contracts traded on commodity exchanges where buyers and sellers agree to exchange a specified quantity of sugar at a predetermined price on a future date. These contracts serve as essential risk management tools for producers, consumers, and traders in the global sugar market.

Major Sugar Futures Contracts

The global sugar market trades several types of sugar futures contracts across different exchanges:

- Sugar No. 11 (Raw Sugar): Traded on the Intercontinental Exchange (ICE), it is the world benchmark for raw sugar trading. Each contract represents 112,000 pounds (50.8 metric tons) of raw centrifugal cane sugar. These contracts are quoted in US cents per pound.

- Sugar No. 5 (White Sugar): Also traded on ICE, these contracts represent refined white sugar. Each contract covers 50 metric tons of white sugar and is quoted in US dollars per metric ton.

- Sugar No. 16 (Domestic Raw Sugar): Traded on ICE, this contract represents raw cane sugar deliverable domestically within the United States. Each contract represents 112,000 pounds and is quoted in US cents per pound. These contracts reflect the U.S. domestic market which operates under a quota system.

- CN-ZCE (White Sugar): Traded on the Zhengzhou Commodity Exchange (ZCE) in China, these contracts represent white sugar with contract size of 10 metric tons and are quoted in Chinese Yuan (CNY) per ton. These are significant for participants interested in the Chinese sugar market.

Factors Influencing Sugar Futures Prices

Sugar futures prices are influenced by a combination of supply, demand, and macroeconomic factors that shape market expectations. Supply-side factors include weather conditions in key producing countries like Brazil, India, and Thailand, which impact crop yields and overall production levels. Government policies, such as export restrictions or subsidies, can also significantly affect global sugar availability.

On the demand side, economic growth, changing consumer preferences, and industrial usage—particularly in food processing and biofuels—drive market trends.

Additionally, macroeconomic factors like currency fluctuations (especially the US dollar), energy prices, and interest rates play a crucial role in determining sugar futures prices. Geopolitical events can also disrupt trade flows, leading to sudden price volatility. These interconnected factors create a dynamic market where futures prices constantly adjust to reflect new information and expectations.

Sugar Futures Prices vs. Sugar Spot Prices

The Difference between Sugar Spot Prices and Sugar Futures Prices

- Sugar Spot Prices refer to the current market price at which sugar can be bought or sold for immediate delivery. These prices reflect real-time supply and demand conditions in physical markets.

- Sugar Futures Prices represent the expected value of sugar at a specified future date. These prices incorporate current market information plus expectations about future supply and demand factors.

Benefits of Comparing Sugar Spot Prices and Sugar Futures Prices

What are the benefits of comparing spot prices with futures prices? It depends on your role in the market, but when you compare these prices, you’re essentially looking at the basis risk—the risk that the difference between the spot price and the futures price (known as the “basis”) might change unexpectedly. This risk is important because it can affect the effectiveness of hedges, trading strategies, and other financial decisions.

The basis risk arises from:

- Geographic differences (production location vs. delivery location)

- Quality variations between the physical sugar and the standardized contract specifications

- Timing mismatches between when hedging is needed and available contract months

The relationship between spot and futures prices provides important information about market conditions. A large premium of futures over spot (contango) often indicates abundant supply, while a discount of futures to spot (backwardation) often signals tight supplies. Changes in this relationship can be early indicators of shifting market fundamentals.

As futures contracts approach expiration, the difference between spot and futures prices influences decisions about whether to make/take physical delivery or close positions. If spot prices are significantly higher than futures prices at expiration, it may be more profitable to buy futures and take delivery rather than buy in the spot market.

How Different Market Participants Use Basis Information

Looking at our example chart comparing Brazilian Santos FOB raw sugar prices (green line) with Sugar No. 11 futures (blue line), we can see how different market players would approach basis risk:

Sugar Producers/Exporters (e.g. Brazilian Mills):

- Monitor the basis to determine optimal timing for hedging decisions

- When the basis widens (as in mid-December), they might accelerate physical sales while maintaining futures hedges

- When the basis narrows (as in late January), they might focus on futures sales rather than physical transactions

- Use basis patterns to negotiate more favorable pricing terms with buyers

Sugar Importers:

- When the basis is narrow (as in mid-February), they might favor buying physical sugar while selling futures for protection

- During wide basis periods (early December), they might buy futures and wait for basis normalization before securing physical supply

- Structure purchasing agreements incorporating basis expectations to optimize procurement costs

Sugar Traders:

- Exploit basis inconsistencies through basis trading strategies

- When the basis expands beyond historical norms, they might establish “short basis” positions (buying futures, selling physical)

- When the basis contracts, they might take “long basis” positions (selling futures, buying physical)

- Utilize historical basis data to identify seasonal patterns and anomalies

Sugar Futures Prices vs. Sugar Forward Prices

The Difference between Sugar Forward Prices and Sugar Futures Prices

- Sugar Forward Contracts are customized, private agreements between two parties to buy or sell sugar at a specified future date at a price agreed upon today.

- Sugar Futures Contracts are standardized agreements traded on regulated exchanges with specific terms regarding quantity, quality, delivery time, and location.

Key Differences:

- Customization: Forwards are tailored to specific needs; futures have standardized terms

- Counterparty Risk: Forwards carry direct counterparty risk; futures are guaranteed by clearinghouses

- Liquidity: Futures are highly liquid with daily market pricing; forwards are typically held until maturity

- Regulation: Futures are regulated and traded on exchanges; forwards are private contracts

Benefits of Comparing Sugar Forward Prices and Sugar Futures Prices

What are the benefits of comparing forward prices with futures prices? The comparison provides valuable insights for market participants making decisions about hedging, trading, and procurement strategies. When looking at these two pricing mechanisms, market participants are analyzing:

- Price Differential: The spread between forward and futures prices may reveal market inefficiencies or regional supply/demand dynamics

- Term Structure: How prices change across different delivery periods in both markets

- Premium/Discount Relationships: Whether forwards are trading at premiums or discounts to futures for similar delivery periods

- Flexibility Value: The premium paid for customization in forward contracts versus standardized futures

How Different Market Participants Use Sugar Forward Price vs. Sugar Futures Price Comparisons

Looking at our example charts comparing Brazilian FOB Brazil forward prices (Image 1) with Sugar No. 11 futures (Image 2) for April 2025 delivery, we can observe that the April 2025 forward price for Brazilian raw sugar is 384 EUR/MT while the April 2025 futures price for Sugar No. 11 is 392 EUR/MT. This 8 EUR/MT difference represents the market’s valuation of standardization, liquidity, and geographic basis. Here’s how:

- Standardization – Sugar No. 11 futures contracts trade on an exchange and have strict quality, delivery, and contract specifications. In contrast, FOB Brazil forward contracts might have variations in quality, shipment terms, and counterparty risk. The additional cost in the futures price reflects the market’s preference for a standardized, predictable contract.

- Liquidity – Sugar No. 11 futures are highly liquid, meaning they are actively traded with many buyers and sellers, making it easier to enter and exit positions. Forward contracts, like those for Brazilian raw sugar, may be less liquid, leading to a discount.

- Geographic Basis – Sugar No. 11 is a global benchmark price, while the Brazilian FOB price is specific to sugar loaded at Brazilian ports. The difference in pricing reflects factors such as freight costs, regional supply-demand dynamics, and the cost of delivering sugar from Brazil to a global destination.

Looking at our example chart comparing Brazilian FOB Brazil forward prices with Sugar No. 11 futures for April 2025 delivery, we can see how different market players would differ in their strategy:

Sugar Producers/Exporters (e.g. Brazilian Mills):

Sugar producers typically prefer selling their sugar using forward contracts because they involve physical delivery and allow them to lock in a price directly with buyers. In contrast, Sugar No. 11 futures contracts are primarily used for hedging and price discovery rather than direct physical sales.

However, producers may still engage with futures markets strategically:

- If futures prices are higher than forward prices, producers might hedge by selling futures contracts and then later arranging a physical sale at a forward price. This allows them to capture a better price while managing price risk.

- If forward prices are higher, it makes more sense to sell directly using forward contracts.

In this example, the April 2025 forward price (384 EUR/MT) is lower than the futures price (392 EUR/MT). This suggests that producers might consider selling futures instead of forward contracts, especially if they expect to buy back futures or deliver locally at better terms.

Sugar Importers/Refiners (e.g., Large Industrial Buyers, Refining Companies):

Importers and refiners compare forward and futures prices to assess procurement timing and cost efficiency.

- If forward prices are lower than futures prices (as in this case, 384 EUR/MT vs. 392 EUR/MT), they may prefer securing physical supply through forward contracts to lock in a better purchase price.

- If futures prices are lower than forward prices, they might wait or hedge their risk by purchasing futures contracts, expecting to buy physical sugar later at a more favorable price.

- Refiners also use futures to hedge refining margins, ensuring stable raw sugar costs relative to refined sugar sales prices.

Sugar Futures Prices vs. AI-driven Forecasted Sugar Prices

The Difference between AI-driven Forecasted Sugar Prices and Sugar Futures Prices

Sugar AI-driven forecasted prices and sugar futures prices serve different purposes in the market, but both provide valuable insights into price trends.

- AI-driven forecasted prices use historical data, machine learning algorithms, and real-time market conditions to predict future sugar prices. These forecasts help market participants anticipate price movements based on statistical models rather than actual trade data.

- Sugar futures prices represent the market’s current expectations of future sugar prices based on live trading activity. These prices are determined by supply-demand dynamics, speculative trading, and hedging strategies of producers, refiners, and traders.

Benefits of Comparing AI-Driven Forecasted Prices and Sugar Futures Prices

Comparing AI-driven forecasted prices with sugar futures prices provides key insights for market participants looking to optimize their trading, hedging, and procurement strategies. The main benefits include:

Market Sentiment vs. Data-Driven Prediction:

- Futures prices reflect real-time market expectations, incorporating speculation, macroeconomic trends, and supply-demand shifts.

- AI-driven forecasts rely on historical patterns, seasonal trends, and statistical analysis, providing an alternative outlook.

- Benefit: Comparing both can help validate market sentiment against fundamental trends, reducing the risk of overreliance on speculative movements.

Identifying Pricing Discrepancies and Arbitrage Opportunities:

- If forecasted prices are higher than futures prices, it may indicate undervaluation in the futures market, suggesting a buying opportunity.

- If futures prices are higher than forecasted prices, it could signal speculative overpricing.

- Benefit: Traders can take advantage of potential mispricings for arbitrage or risk-adjusted trading strategies.

Enhancing Hedging and Procurement Decisions:

- If an AI forecast predicts a price drop while futures prices remain high, a buyer may delay purchases to secure a better price.

- Conversely, if forecasts predict a price increase, buyers may lock in futures contracts earlier to hedge against rising costs.

- Benefit: Comparing both tools allows for more informed risk management and purchasing decisions.

Longer-Term Visibility Beyond Futures Contracts:

- Futures prices are limited to contract expirations (e.g., Aug 2025), whereas AI-driven models can extend beyond active futures contracts to offer insights into longer-term pricing.

- Benefit: Helps participants plan beyond available futures contracts, especially for long-term budgeting and investment planning.

How Different Market Participants Use AI Forecasts vs. Futures Prices

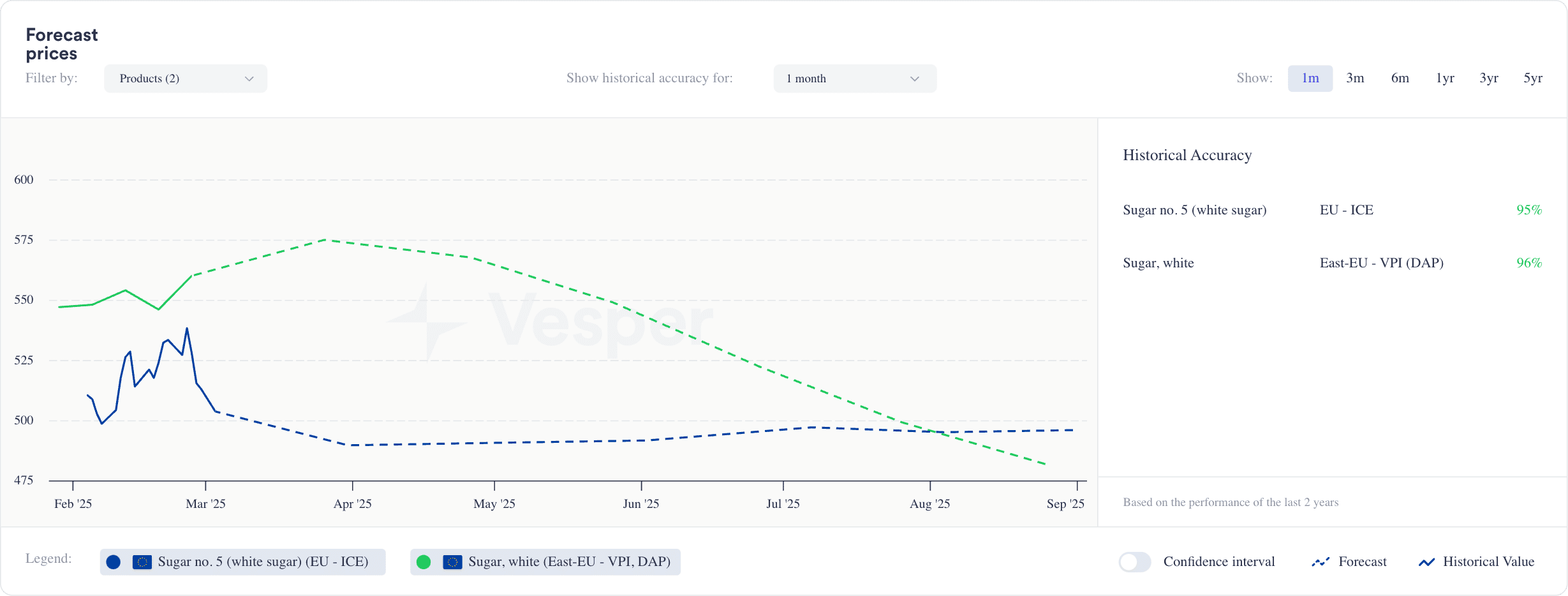

Looking at our example charts comparing AI-driven forecasted price for East-EU White Sugar (VPI, DAP) (image 1), with Sugar No. 5 Futures price (image 2), we can observe that the AI-driven forecasted price for East-EU White Sugar (VPI, DAP) is 481 EUR/MT for August 2025, and the Sugar No. 5 Futures price for August 2025 is 470 EUR/MT. This 11 EUR/MT difference suggests that futures prices are trading lower than the AI model’s expectations. Here’s how different participants might interpret and act on this:

Sugar Producers & Exporters:

- Producers use futures markets for hedging and price discovery.

- Since futures prices (470 EUR/MT) are lower than forecasted prices (481 EUR/MT), producers might believe the market is undervaluing future sugar supply.

- Potential Action: A producer may delay forward sales, expecting futures prices to rise toward AI-forecasted levels.

Sugar Importers & Refiners:

- Importers and refiners compare futures and forecasted prices to time purchases efficiently.

- Seeing a lower futures price (470 EUR/MT) compared to the AI forecast (481 EUR/MT), an importer might secure futures contracts now at a lower cost before prices potentially increase.

- Potential Action: Lock in futures contracts early to hedge against expected price increases.

Traders & Speculators:

- Traders monitor discrepancies to find arbitrage or trading opportunities.

- The 11 EUR/MT difference could suggest futures are undervalued, prompting a trader to go long on futures (buy contracts) and hold until prices align with AI predictions.

- Potential Action: Buy futures at 470 EUR/MT, anticipating an upward correction toward the AI forecasted price of 481 EUR/MT.

Conclusion

The global sugar futures market offers multiple pricing mechanisms that serve distinct yet complementary purposes for industry participants. Sugar spot prices provide real-time market conditions, futures contracts standardize risk management, forward contracts offer customized physical delivery terms, and AI-driven forecasts deliver data-based predictions that may identify market inefficiencies. Understanding the relationships between these pricing mechanisms—such as basis risk, contango versus backwardation, and price convergence patterns—reveals crucial information about market fundamentals. Brazilian producers, European refiners, and global traders each benefit from analyzing these price relationships in different ways, allowing them to optimize hedging strategies, procurement timing, and arbitrage opportunities.

FAQ

1. How Can I Trade Sugar Futures?

Sugar futures are primarily traded on the Intercontinental Exchange (ICE). To trade sugar futures, participants must:

- Open an account with a registered broker or trading platform

- Meet margin requirements (initial and maintenance)

- Select appropriate contract months based on hedging or trading objectives

- Monitor positions and manage risk accordingly.

2. What Are the Risks Associated with Trading Sugar Futures?

While sugar futures can be a powerful tool for managing risk, they also come with significant risks. One of the main risks is market volatility; if the market moves against your position, you could face substantial losses. Additionally, trading on margin (borrowing money to trade) can amplify these losses, potentially leading to a margin call, where you must add more funds to maintain your position. There’s also the risk of liquidity—if you need to exit a position quickly, you might not be able to find a buyer or seller at your desired price. Lastly, because futures contracts have expiration dates, there’s a risk of having to take physical delivery of the commodity if the contract is not closed or rolled over in time.

3. What is a Long Hedge in Sugar Trading?

A long hedge is a risk management strategy used by sugar processors, food manufacturers, and other buyers to protect against rising sugar prices. When a company expects that sugar prices will increase in the future, it buys sugar futures contracts to lock in current prices and avoid paying higher costs later. For example, a candy manufacturer that needs sugar for production may purchase Sugar No. 11 futures at today’s price to hedge against potential price surges due to poor harvests or supply chain disruptions. If sugar prices rise as expected, the gains from the futures position offset the increased cost of physical sugar purchases, ensuring stable production costs.

4. What is a Short Hedge in Sugar Trading?

A short hedge is used by sugar producers or exporters to protect against declining sugar prices. By selling futures contracts, they secure a price for future sales, mitigating the risk of price drops before their physical sugar is sold in the market. For example, a Brazilian sugar mill expecting to ship sugar in six months might sell Sugar No. 11 futures today at 18 cents per pound. If market prices fall to 16 cents per pound by the time the sugar is ready for sale, the loss in the physical market is offset by gains in the futures position, ensuring a more predictable revenue stream.

5. What is Spread Trading in Sugar Trading?

Spread trading involves taking advantage of price differences between two related futures contracts, either in different contract months or between different sugar types. Traders may execute an intermonth spread, where they buy a near-term contract and sell a later-term contract, betting on price changes between the two. Alternatively, they may engage in an intercommodity spread, trading the price difference between raw sugar futures (Sugar No. 11) and refined sugar futures (Sugar No. 5). For example, if raw sugar futures are expected to rise faster than refined sugar futures due to a supply shortage, a trader might buy Sugar No. 11 futures while simultaneously selling Sugar No. 5 futures to capture the price differential.

6. What is Trend Following in Sugar Futures Trading?

Trend following is a strategy where traders identify and trade in the direction of prevailing price trends. This involves using moving averages, momentum indicators, and price action patterns to determine whether sugar prices are in an uptrend (bullish) or downtrend (bearish). For example, if sugar prices have been steadily increasing over the past few months, a trend-following trader might buy Sugar No. 11 futures in anticipation of continued upward momentum, setting stop-losses to manage risk in case the trend reverses.

7. What is Seasonal Trading in Sugar Markets?

Seasonal trading capitalizes on historical price patterns that repeat due to factors such as harvest cycles, weather conditions, and demand fluctuations. Sugar prices often rise before peak harvesting seasons and decline post-harvest as supply increases. For example, sugar production in Brazil typically ramps up in April-May, leading to lower prices due to increased supply. A trader using a seasonal strategy might short sugar futures in March in anticipation of post-harvest price declines.

8. What is Fundamental Analysis in Sugar Trading?

Fundamental analysis involves evaluating sugar market dynamics based on supply and demand factors, weather conditions, production estimates, and government policies. Traders monitor key reports such as USDA crop forecasts, Brazilian export data, and Indian government subsidies to predict price movements. For example, if a drought in India reduces sugarcane production, a fundamental trader may expect sugar prices to rise and buy Sugar No. 11 futures in anticipation of a supply-driven rally.

9. What is Technical Analysis in Sugar Futures Trading?

Technical analysis relies on price charts, indicators, and patterns to predict future price movements in sugar futures. Traders use tools like moving averages, RSI (Relative Strength Index), and Fibonacci retracements to identify entry and exit points. For example, if Sugar No. 5 futures price forms a “double bottom” pattern—a bullish reversal signal—traders may buy futures contracts expecting an upward breakout. Conversely, if prices break below a key support level, a trader might sell or short futures contracts, anticipating further declines.

10. What is Basis Risk in Sugar Trading?

Basis risk in sugar trading refers to the uncertainty in price movements between the physical sugar market and the sugar futures market. The basis is the difference between the local cash price of sugar (the price at which physical sugar is bought or sold in a specific region) and the futures price of sugar (the price of a standardized sugar contract traded on an exchange like ICE). If this difference fluctuates unexpectedly, it creates basis risk for market participants.

For example, a sugar producer in Brazil may hedge by selling Sugar No. 11 futures at 20 cents per pound while expecting to sell physical sugar at a small discount of 0.5 cents per pound (basis = -0.5). However, if local sugar prices drop more than expected due to an oversupply, the basis could widen to -1.5 cents per pound, meaning the producer receives a lower-than-expected final price for their sugar. Even though the hedge remains in place, the unexpected change in the basis results in a financial risk.